1. Introduction

Small and medium enterprises (SMEs) play a prominent role in the Indonesian economy, contributing to job creation and poverty alleviation within Indonesia and abroad (Nursini, 2020). Some studies also remarked that SMEs are the foundation for economic growth and the development of nations (Abisuga-Oyekunle et al., 2019; Surya et al., 2021). At the same time, the productivity of SMEs generated a growing negative trend during and post-COVID-19 (Ragazou et al., 2022). SMEs are frequently reported to have had a bigger impact on the pandemic, and the Indonesian government and other countries have responded to integrate technology into the production and distribution processes (Bai et al., 2021; Hidayati & Rachman, 2021). However, the absence of literacy and knowledge will make it difficult to support productivity (Ismanto et al., 2020).

With growing recognition of the pivotal role of knowledge and literacy, knowledge-based view (KBV) is gaining prominence within the business and management communities (Grant & Phene, 2022). KBV posits that a firm’s knowledge, including its tacit and explicit knowledge assets, is a critical source of competitive advantage (Gassmann & Keupp, 2007). Thus, SMEs are increasingly prioritizing knowledge management, fostering literacies, and investing in technologies that facilitate knowledge sharing and dissemination to fully capitalize on their knowledge resources (Lee, 2016). In this study, we involved two possible knowledge-based resources which are relevant to supporting SMEs productivity, including financial literacy and digital literacy.

Digital literacy has raised significant interest among business and scholars in recent years (Ollerenshaw et al., 2021; Widiastuti et al., 2021). This is essential in the twenty-first century, as business activities are required to incorporate technology. Some scholars remarked that the growing interest in digital literacy in SMEs is primarily persuaded by its authorizing nature, with its essential advantages being the diminishing of restrictions (Dura, 2022; Molina-Garcia et al., 2023). In addition, another study noted that digital literacy is essential as the antecedent for technological usage in the activities of SMEs, such as marketing (Malodia et al., 2023). Recent studies have witnessed that the vulnerable impact of SMEs during and after the COVID-19 pandemic is due to the curve in technological transition (Fan & Ouppara, 2022). Thus, the enhancement of digital literacy will be forecasted to promote technological usage, which can further boost their productivity (Ollerenshaw et al., 2021).

In addition to digital literacy, financial literacy is a prominent knowledge resource for promoting the capacity, skills, and attitudes of SMEs that can lead to productivity (Rahmawati et al., 2023). Several preliminary studies remarked that sufficient financial literacy has a connection to SMEs innovation and performance (Hutahayan, 2021; Kulathunga et al., 2020). Another study linked the prominent role of financial literacy on capital resources that can help SMEs succeed (Yakob et al., 2021). Thus, it is necessary to comprehend how financial literacy stimulates the capacity of business owners to access digital support for business sustainability. Hence, this present study stipulates a detailed analysis of financial literacy and digital literacy and examines the pathways through which marketing intensity can promote SMEs performance.

This research is posited to provide several indispensable insights into the field of entrepreneurship and the development of SMEs, with some forecasted contributions as follows. First, while almost numerous papers are concerned with examining the productivity of SMEs through human resources lenses and organizational matters (e.g., Harney & Alkhalaf, 2021; Hernita et al., 2021; Sawaean & Ali, 2020), this study incorporated the light from KBV to bridge the link between financial literacy and digital literacy in the small-medium business literature. Second, this present research is forecasted to significantly contribute to the entrepreneurship and small-medium business literature by testing the role of marketing intensity on the effect of financial literacy, digital literacy, and small-medium business productivity.

The rest of the paper is provided as follows. First, a brief digest of the link between the variables of the study is provided in Section 2. Next, the methodological approach to dealing with research hypotheses is presented in Section 3. In addition, the results obtained from the statistical outputs are explained in Section 4 and followed by the discussion in Section 5. This paper ends with conclusions, implications, and limitations.

2. Literature Review

2.1. Financial Literacy

The knowledge-based view (KBV) pointed out the prominent of tangible and intangible assets in resulting competitive advantages for small and medium enterprises (SMEs) (Heenkenda et al., 2022). Almost all studies only concern on examining the antecedents of SMEs productivity or performance, ignoring the role of literacies (e.g., Prasanna et al., 2019; Purwati et al., 2021; Sawaean & Ali, 2020). This study assumed that the KBV can be used to understand how literacies can promote marketing intensity and business performance. In addition, KBV seeks to explain how SMEs should perform a thorough internal analysis to identify and evaluate their resources and capabilities, including financial and digital literacy (Kulathunga et al., 2020). Financial literacy has been acknowledged by scholars as its role in helping to promote financial decisions to support business performance and productivity (Agyei, 2018). Some studies also remarked that financial literacy escalates the productivity of SMEs in this complicated business circumstance based on knowledge (Lenggogeni & Usman, 2023; Wijayanto et al., 2020). In addition, preliminary papers argued that financial literacy is better equipped to allocate its financial resources strategically in small-medium businesses, enabling it to invest more effectively in marketing efforts (Saifurrahman & Kassim, 2021). Thus, the first set of hypotheses is described as below.

H1. Financial literacy has an impact on SMEs productivity

H2. Financial literacy has an impact on marketing intensity

2.2. Digital Literacy

Digital technology, starting with computerization and the use of the internet, is something that cannot be avoided by managers of small and medium industries, from urban to rural areas. Concerning Indonesia, the government has developed smart villages based on internet networks (Irmayani et al., 2022). In short, when market capacity in the surrounding area weakens, the product can be absorbed by other markets. Digital literacy has the implication that SMEs can involve technology in production and distribution activities, such as involving technology in marketing (Widiastuti et al., 2021). For small and medium industries in Indonesia, digitalization has not yet taken place in the production process because production technology is still simple and involves workers from the surrounding environment (Asiati et al., 2018). However, related to the pandemic period, the quality of managers in the field of digitalization has indeed proven to cause SMEs to survive. Some studies (e.g., Erlanitasari et al., 2020; Karim et al., 2021; Viswanathan & Telukdarie, 2021) observed that financial literacy and digital literacy can significantly increase the financial preference capabilities of the industry, which in turn can promote productivity. Thus, the second set of hypotheses is described below.

H3. Digital literacy has an effect on SMEs productivity

H4. Digital literacy has an impact on marketing intensity

2.3. Marketing Intensity and SMEs Productivity

The marketing of SMEs is prominent in enhancing productivity (Hernita et al., 2021). Marketing intensity ensures that higher effort for marketing purposes will beneficial in raising the SMEs productivity (Surya et al., 2021). For instance, marketing intensity (e.g., advertising, social media usage) can escalate the visibility and image of SMEs among its target audience (Dwivedi et al., 2021). Some preliminary papers remarked that marketing intensity is considered an effective strategy to encourage business performance or productivity (e.g., Acikdilli et al., 2022; Giantari et al., 2022). Scholars suggested that marketing intensity will promote to increased investment in marketing efforts, such as advertising, promotions, and customer outreach (Markovitch et al., 2020). It allows SMEs to enhance their market, which can lead to increased sales, customer loyalty, and market share. Furthermore, marketing strategy usage can help SMEs adapt to market changes and identify new opportunities, which contribute to overall productivity (Giantari et al., 2022). Accordingly, the hypothesis is provided below.

H5. Marketing intensity and SMEs productivity

2.4. Marketing Intensity as a Mediator

Marketing intensity is commonly regarded as a fundamental result of business strategy. Some preliminary papers adopted knowledge-based value (KBV) to understand SMEs productivity (e.g., Duarte Alonso et al., 2022; Schoenherr, 2022). Financial literacy has been considered an internal resource for SMEs to promote marketing intensity (Yakob et al., 2021). In this regard, more capable business actors with financial and digital literacy will promote informed decisions about resource allocation. Some studies have noticed that marketing intensity can better assess the potential returns and their financial resources more strategically (Santini et al., 2019). However, there is still a gap to identify the mediating role of marketing intensity between financial literacy, digital literacy, and SMEs productivity. This present research draws the positive connectivity of marketing intensity as a mediator through KBV. A prior study Diptyana & Herlina (2022) mentioned that studies exploring the outcomes of SMEs productivity often use KBV to understand the presence of the link between financial literacy and digital literacy. In other words, marketing intensity can serve as mediators that receive the effects of financial literacy and digital literacy, which in turn impact the productivity of SMEs. Therefore, the last set of hypotheses is presented as follows.

H6. Marketing intensity mediates the linkage between financial literacy and SMEs productivity

H7. Marketing intensity mediates the linkage between digital literacy and SMEs productivity

3. Research Method

3.1. Design and Participants

This research used a quantitative approach with partial least squares structural equation modeling (PLS-SEM) statistical tests to analyze the influence of financial literacy, digital literacy, and SMEs productivity, as well as to confirm the role of marketing intensity as a mediator. The research took place in the East Java region, which consists of three districts or cities, namely Gresik regency, Pasuruan regency, and Mojokerto city, because this area is included in the area that contributes the largest economic income in East Java, namely 63% compared to other areas, and considering the large number of SMEs industries developing in this area. The number of samples was taken proportionally by random sampling, which is a snapshot of the entire population of SMEs in the district or city.

SMEs are one of the industries that are increasingly growing in the region and are being used as an icon of regional economic growth. The number of respondents was 232 small and medium-sized industry managers. In terms of business scale, the majority of SMEs are involved in small scale (76.7%), and they are also concerned with the culinary sector (65.6%). In addition, the majority of SMEs have business experience less than three years (38.8%), followed by SMEs with experience more than 10 years (25%). The data further showed that 90.05% of SMEs actors were graduates of senior high school, and small percentages were university graduates. The average income of SMEs was less than IDR 100 million per year.

3.2. Measures

Financial literacy is stipulated as awareness, knowledge, and skills in managing finances. We involved six indicators from van Rooij et al. (2011); Bongomin et al. (2017) to measure financial literacy, namely awareness, knowledge, and skills about money and income, payments and bills, prices and financial records, financial planning, saving, and debt, investment, and fraud. Digital literacy is measured by the level of understanding of entrepreneurs regarding the use of digital media and social media to market products and we followed indicators from Sulistyowati (2021). Marketing intensity is how often and what marketing variants are carried out by SMEs. In this research, we involved four indicators from Bae et al. (2017), including print media, electronic media, social media, and online marketplaces. Lastly, the productivity of SMEs is measured before, during, and after. The indicators are turnover, number of customers, and number of units sold. We adopted items from Kulathunga et al. (2020) to measure SMEs productivity. All items of the questionnaire have been provided through closed-ended questions in a Likert’s scale ranging from 1=strongly disagree to 5=strongly agree to calculate the degree of perceptions among respondents.

3.3. Data Analysis

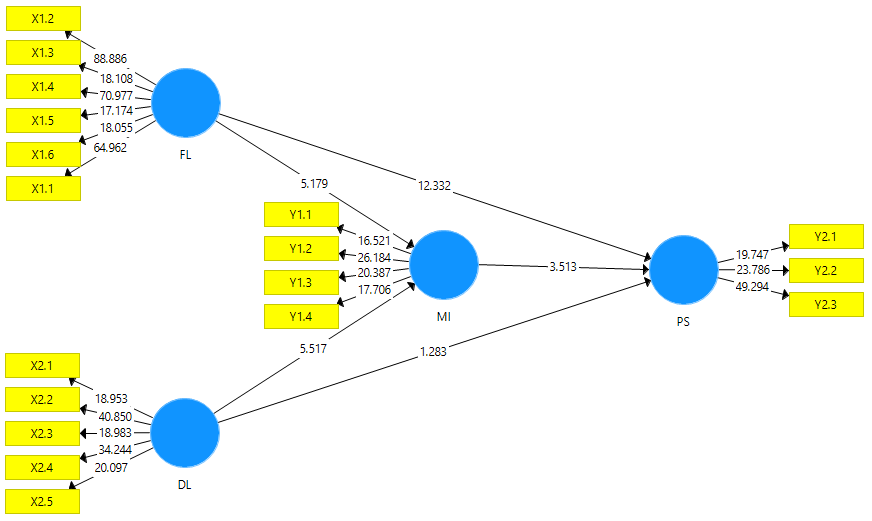

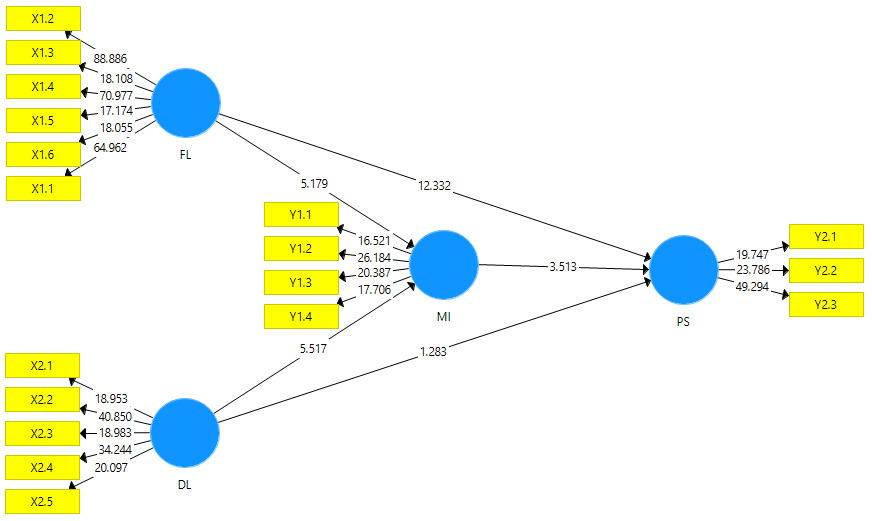

After the data is collected, the analysis technique used is partial least squares structural equation modeling (PLS-SEM) by first determining the path trajectory (path analysis) as shown in Figure 1. In this figure, apart from having the same goal, namely measuring the existence of path trajectories, the choice to use Smart-PLS version 3.0 is that it does not have to be bound by assumptions, including the need for normal distribution. However, the question items as support for variable indicators have been tested for validity and reliability. After that, these values are collected as indicators of each variable.

4. Results

4.1. Outer Model Assessment

To estimate the outer model (measurement model), the recommended threshold of the loading factor should be more significant than (> .6), the average of extracted value (AVE) should higher than (> .5) and the composite reliability should greater than (> .6) (Hair et al., 2019). Table 2 illustrates that the loading factor for the latent variables ranges from .71 to 0.92 (> .6), while AVE value ranges from .58 to .68 (> .5), and the CR value ranges from .75 to .91. These results indicate that the model has meet the internal consistency and convergent validity. In addition, this study also performed discriminant validity. Table 3 demonstrates that AVE’s square root value was more outstanding than the construct correlation scores, concluding that the scores met the imperative for discriminant validity (Hair et al., 2019).

4.2. Inner Model Evaluation

This research uses the R-square (R2) to show the closeness of model predictions. It computes how well an exogenous variable explains an endogenous construct. Hair et al. (2019) estimates R2 to be between 0 and 1. R2 values above .75 mean it is large, whilst .50 and .25 mean it is small and weak. Calculations showed that FL and DL explained 52.6% of the MI variance with reasonable predictability. FL, DL, and MI account for 80.9% of the PU variance with reasonable predictability. Next, f2 indicates whether the foreign construct influences the endogenous construct. As stated by Hair et al. (2019), external constructions have minimal, moderate and significant impact on endogenous constructions with f2 values of .02, .18 and .40. In particular, the effect size of FL and DL on MI was quite large (f2 = .16). The magnitude of the impact of FL, DL, and MI on PU is also significant (f2 = .16).

4.3. Hypothesis Testing

Table 4 and Figure 1 demonstrates that financial literacy and SMEs productivity relationship was significant (β = .70), supporting H1. Besides, FL significantly affected marketing intensity (β = .39), accepting H2. At the same time, digital literacy affected SMEs productivity (β = .06) and marketing strategy (β = .34), supporting H3 and H4. Moreover, the direct impact of marketing intensity on SMEs performance (β = 0.2), accepting H5. For the mediating analysis, we followed the suggestion from Hayes (2009) by comparing the direct effect before and after the mediator enter into the model. As illustrated in Table 4, MI failed in mediating DL and PS since the there is no direct influence of DL and PS, thus not supported H6. Lastly, the mediating role of MI between FL and PS was proposed in H7; this hypothesis was confirmed since there is a change in the coefficient value (β = .081, T-value = 3.159, p < .05). Thus, the presence of mediator makes the p-value still significant, thus it can be concluded as a partial mediation.

5. Discussion

First, this study reported that financial literacy played significant role on small-medium enterprises (SMEs) productivity and marketing intensity. This suggests that financial literacy is robust predictor for actual business productivity and marketing strategy. The findings validate the previous works (e.g., Aldi et al., 2019; Sariwulan & Suparno, 2020; Viswanathan & Telukdarie, 2021) which showed that SMEs involve their productivity through financial literacy. This also reinforces with research that has been conducted by Sulistyowati (2021); Yuesti et al. (2020) which described problems in the business, including problems and provide alternative solutions for marketing strategy. Some studies also remarked that financial literacy escalates the productivity of SMEs in this complicated business circumstance based on knowledge. In addition, preliminary papers argued that financial literacy is better equipped to allocate its financial resources strategically in small-medium businesses, enabling it to invest more effectively in marketing efforts.

Second, the statistical output indicated that digital literacy has a significant effect on SMEs productivity and marketing strategy. The findings support several studies (e.g., Omar et al., 2020; Sariwulan et al., 2020) which remarked that digital literacy for SMEs will encourage creativity to become entrepreneurs and develop their business capabilities. It enables SMEs to utilize e-commerce features to be used wisely and productively to increase marketing. Even though the productivity of SMEs can increase with digital literacy and the involvment of technology in the business world, in fact in this research the productivity of SMEs has not yet experienced a significant increase considering the lack of digital literacy. This is a new discovery in line with research results (Fauzi et al., 2021; Islami et al., 2021; Sariwulan & Suparno, 2020).

In addition, this study also found that a robust link between marketing intensity and business productivity. The basic rationale to brace this result is that marketing intensity ensures that higher effort for marketing purposes will beneficial in raising the SMEs productivity (Surya et al., 2021). For instance, marketing intensity (e.g., advertising, social media usage) can escalate the visibility and image of SMEs among its target audience (Dwivedi et al., 2021). This study confirmed some preliminary papers which remarked that marketing intensity is considered an effective strategy to encourage business performance or productivity (e.g., Acikdilli et al., 2022; Giantari et al., 2022).

Furthermore, digital literacy has a significant influence on SMEs productivity through marketing intensity. The research results show that SMEs have a creative environment and professional and competitive human resources. These results confirm initial research which shows that SMEs need digital and financial literacy support as well as marketing intensity support. Digital literacy, financial literacy, and marketing intensity can help individual to study and well-informed about competition and estimate the productivity of SMEs. The finding supports preliminary studies (e.g., Erlanitasari et al., 2020; Sulistyowati, 2021; Toruan et al., 2021). SMEs’ productivity can find out developments in business conditions with technological developments that they can follow, namely digital literacy and digital finance. Marketing intensity support allows SMEs to respond to competition and develop the company to gain profits.

6. Conclusion

This research investigates the relationship between financial literacy, digital literacy, marketing intensity and the productivity of SMEs in Indonesia. These findings show that financial literacy and digital literacy can explain the productivity of SMEs. Indeed, marketing intensity can mediate between financial literacy, digital literacy and SMEs productivity. This research emphasizes the impact of literacy and technological developments for SMEs in daily life related to marketing intensity.

6.1. Implications

This present study makes several practical and theoretical contribution. First, there is demanding research on small-medium enterprises, while focusing on financial literacy and digital literacy received a scant consideration. Thus, this study will provide theoretical contribution on entrepreneurship and small-medium business based on knowledge-based resource and help to strengthen the role of marketing intensity in linking literacies and productivity of SMEs. In lens of practical, there is a prominent role of marketing intensity so that SMEs can touch this matter and enhance to innovate for their marketing strategy. In addition, there is a need of several trainings to increase the productivity of SMEs conducted by the government, and they can also learn from several social media channels, which provide a lot of learning and know product trends and current competitive conditions.

6.2. Limitation and Future Direction

Despite this research made some practical and theoretical contributions, it is essential to acknowledge limitations and identify future directions. First, this study involved a self-administered survey in which it has potential for bias. Thus, further scholars can elaborate a combination between online and offline questionnaires to obtain better results. In addition, one of the main obstacles to this research is related to the geographic sampling strategy, which exclusively targets the East Java level. Therefore, further researchers can explore the subject matter further within a more comprehensive investigation framework.