Introduction

Access to capital is critical for entrepreneurial success. A founder often requires external start-up and operational funding, in addition to funding across critical growth stages. However, it is well documented that minority and female founders experience greater difficulty accessing capital to support their entrepreneurial ventures relative to non-minority founders (Becker–Blease & Sohl, 2011; Coleman & Robb, 2009; Kanze et al., 2018; Rouse & Jayawarna, 2006). While factors such as disadvantageous geography and distribution channels, lower annual receipts, and relatively limited business exposure and acumen are referenced as hinderances to minority and female entrepreneur success (US Department of Commerce, 2010), inequitable access to capital is commonly cited and recognized as a significant contributor to the higher failure rates and restricted growth of these businesses (Astebro & Bernhardt, 2003; Robb & Fairlie, 2007).

Much evidence implicates bias rooted in the traditional systems that deploy capital, and/or bias on the part of individuals making capital deployment decisions via more traditional funding sources such as banks and venture capital (VC) (Bewaji et al., 2015; Kanze et al., 2018; Voitkane et al., 2019). Accordingly, it is of interest to explore and determine whether non-traditional funding sources offer increased accessibility and funding success for minority and female founders relative to non-minority and male capital seekers.

Further, prior literature incorporating elements of signaling theory (Spence, 1973) provide that entrepreneur characteristics and firm information may reduce investor uncertainty given the presence of information asymmetry. As such, and in line with prior literature (Solodoha, 2024; Solodoha & Blaywais, 2023), we examine whether entrepreneur characteristics provide signals that mitigate this asymmetry, thus increase capital access success.

This paper explores the funding success of Reg CF equity crowdfunding campaigns by minority status and gender. Crowdfunding is a non-traditional funding option that allows founders to source capital from a large crowd of non-accredited investors. This democratization of capital deployment decision making may remove some of the barriers to accessing capital that is reported via more traditional funding sources and ultimately increase the odds of minority and female entrepreneurial success. We also examine whether specific campaign and founder characteristics impact the success of these campaigns and whether crowdfunding is a viable option for reducing the minority and gender funding gap.

Entrepreneurship Impact on the Economy & Wealth

Entrepreneurship is the cornerstone of a healthy and bustling economy. The Small Business Administration (SBA) reports that small businesses account for nearly 44% of US GDP and roughly 46% of all private sector employment. Between 1995-2021, small businesses created over 17 million net new jobs, accounting for more than 62% of said job creation during this period.

Entrepreneurship is also a principal factor in wealth creation and household financial mobility (Quadrini (2005); Bates (1997)). According to the SBA Office of Advocacy, those that are self-employed are wealthier than those that are not[1]. The Federal Reserve Board Survey of Consumer Finance reported that as of 2019, 58% of household assets were non-financial. Business equity accounted for 34% of the total, second only to homeowner equity. These statistics suggest that supporting small business development and growth contributes greatly to domestic economic well-being and the potential for increased net-worth of households with business equity.

Supporting entrepreneurs and small businesses equitably provides economic empowerment and the ability for business owners to contribute to their communities in meaningful ways. As such, inequities leave disenfranchised entrepreneurs and their communities economically disadvantaged.

Minority and Gender Funding Gap

Minority and female entrepreneurs can face significant challenges when seeking capital via traditional funding sources relative to non-minority male entrepreneurs. These headwinds serve as natural impediments to the formation, growth, and ultimate survival of these enterprises.

Fairlie, Robb and Robinson (2022) examine access to capital amongst Black start-ups and find that Black businesses start smaller and stay smaller in size relative to their White counterparts and face more difficulties in raising external capital (especially external debt). This is, in part, attributed to lower credit scores. An additional hinderance is a perception held by some Black founders that traditional capital providers such as banks will likely deny their credit request. As such, these founders choose not to apply for credit, thus operate with sub-optimal funding. Further, the authors find this belief pattern to be the case for Black entrepreneurs with less favorable credit payment histories and those with good credit. This finding is of significance given Astebro and Berhardt (2003) find a positive relationship between business survival and having a bank loan (access to capital) at start-up. This relationship holds after controlling for founder and business characteristics. Thus, Black entrepreneurs who do not seek debt financing, even those with strong credit histories, out of fear of rejection, may start their ventures under-funded, disadvantaged, thus are more likely to fail.

The literature provides multiple theories to explain why minority and female entrepreneurs are less likely to successfully access capital via traditional funding sources and why these businesses are less likely to thrive. Some attribute these differences to borrower risk and investor risk preferences Canning, et. al (2012) and Thebaud (2015). Mason and Harrison (2003) also provide a risk-based explanation, suggesting that some business owners, due to limited business history and limited assets at start-up, fail to signal sufficient creditworthiness. Further, the Census Bureau 2021 Annual Business Survey reported that Asian, Black and Hispanic business owners were more likely to seek credit to cover operating expenses as opposed to financing CAPEX or enterprise growth which drives the ability to service debt.

Guzman and Kacperczyk (2019) examine the gender funding gap in entrepreneurship, or the fact that men-led ventures are more likely to receive external funding than women-led ventures. They conclude that 65% of this gap can be explained by differences in how external investors perceive the growth potential of women-led ventures. Specifically, they posit that women-led ventures are less likely to be perceived as signaling a sufficient growth opportunity, calling to question whether women founders fail to effectively convey the growth opportunity, whether women tend to lead less growth-oriented ventures, or whether external investors, who are likely male, fail to see the growth potential in women-led ventures. This later notion may be attributed, in part, to social role theory (Eagly, 1987), or the notion that information processing, interpretation, and choice outcomes on the part of investors, can be driven and biased by societal and culturally defined roles and expectations (Elitzur & Solodoha, 2021; Serwaah & Shneor, 2024; Shneor et al., 2017).

Notwithstanding the risk argument, significant literature points to bias in the traditional capital funding systems, inclusive of bias by those making credit and capital investment decisions. Coleman (2004) finds that Black men were less likely to receive loan approval when compared to Hispanic, Asian, and White men. This finding held after controlling for firm risk and founder characteristics such as education level. Kanze, et. al (2018) examine the gender gap in venture capital (VC) funding and find that funding disparities are a function of gender bias in the line of questioning asked of female and male founders seeking VC funds. They posit that male founders are presented with ‘promotion-focused’ questions, while women are asked ‘prevention-focused’ questions. They conclude that the likelihood of funding decreases with ever ‘prevention-focused’ question presented to a female founder. Numerous papers report that women encounter more ‘credibility’ bias (Eddleston et al., 2016; Jennings & Brush, 2013). Given that males dominate the VC space (Alsos et al., 2006), embedded gender bias is a major contributor to the gender funding gap (Alsos & Ljunggren, 2017; Coleman & Robb, 2009; Voitkane et al., 2019; Welter & Gartner, 2016). Further, Black start-ups face challenges when seeking debt financing relative to non-Black counterparts (Bates, 1991; Blanchard et al., 2008; Fairlie et al., 2022).

Cagetti and DeNardi (2006) examine entrepreneur outcomes in the face of such financing constraints. They find that founders facing more financing constraints tend to have firms that are, on average, smaller and that these founders have less concentrated wealth. Moreover, these financing constraints restrict the overall number of entrepreneurs. While policy will be critical to ensuring equity in the capital process, identifying an alternative to traditional funding sources would provide an immediate remedy and opportunity for minority and female founders to access the funds needed to start and operate their ventures. Accordingly, these entrepreneurs may realize increased household wealth, the ability to create jobs and positively impact their communities and contribute to overall economic productivity.

Crowdfunding

This analysis examines the viability and potential impact crowdfunding campaigns may have for founders seeking capital and identifies entrepreneur characteristics that may support campaign success. Access to capital is critical to the viability and growth of a business venture. Moreover, where personal savings are lacking, access to external start-up funds is paramount. Altonji and Doraselski (2005) report significant differences in savings rates between Black and White households. Robb and Fairlie (2007) find that Blacks start with 1/11th the wealth of Whites, a disparity making it less likely that Blacks will start a business or have access to personal funds necessary to start a business. Moreover, they find that when entrepreneurs push through this initial impediment, this lack of capital limits growth and the ability to remain a going concern. They also find racial disparities in accessing start-up capital contribute to lower sales and profit, less employment, and higher failure rates. Crowdfunding offers access to capital across various venture stages thus, may provide a means of democratizing access to capital for under-served entrepreneurs.

Crowdfunding campaigns differ from traditional funding sources such as VC and credit granting institutions given that crowdfunding capital is sourced from a large pool of individual investors. Crowdfunding investors are generally not accredited and these campaigns offer decentralized capital access as opposed to more centralized decision making bodies like banks and accredited VC investors. Founders can run a crowdfunding campaign on a crowdfunding platform to source capital, ideally, from a large crowd of investors. During these campaigns founders offer information, via a crowdfunding platform, to potential investors which often includes information about the founder(s), overall business operations, available financials, and potential risks, to name a few. Investors can search the platform and contribute capital to campaigns of their choosing. Via crowdfunding, an investor can contribute as little as $100. Crowdfunding campaigns succeed when founders garner enough attention, interest, and investment traction from the crowd to reach their minimum target raise amount.

Crowdfunding platforms charge fees, which can range from 3% to 10% or more of investment dollars raised, and sometimes take equity stakes in the company. In exchange, platforms provide entrepreneurs access to a crowd of potential investors, and/or a platform to direct a friendly investor crowd. In addition, platforms may provide access to data and various other services, such as due diligence assistance. Given the evidence that minority and female entrepreneurs are less likely to attract debt and equity via more traditional funding sources, we explore whether crowdfunding presents an effective alternative means. Specifically, we attempt to determine whether crowdfunding platforms reduce the funding gap for minority and female entrepreneurs seeking capital, whether gender or minority status impact a founder’s ability to raise minimum campaign targets, and whether founder characteristics impact campaign success.

Nitani, Riding and He (2019), Solodoha and Blaywais (2023), and Solodoha (2024) examine whether and how crowdfunding investors interpret signals and information presented by founders when selecting amongst opportunities. They find that information updating matters, and potential investors, in an attempt to minimize risk, tend to choose larger firms with experienced and educated management, and campaigns that appear to have better growth opportunities. These findings suggest that crowdfunding investors tend to be rational, choosing to minimize risk and maximize returns, and pay attention to project signaling. However, Younkin, and Kuppuswamy (2018) analyze over 7600 crowdfunding projects and find that crowdfunding investors routinely rate projects led by Black men as lower quality when compared to campaigns led by White founders. Further, Black male led campaigns are significantly less likely to receive funding. The authors identify unconscious bias as the driver of this discriminatory practice. Cumming, Meoli, and Vismara (2021) and Singh and Miller (2024) find that minority entrepreneurs do not have higher odds of funding success. However, Cumming et. al (2021) note that minority entrepreneurs do attract more investors.

By contrast, Abrams (2022) finds increasing public and private support for Minority-Owned Business Enterprises (MBEs), including services and access to resources such as education, business development programs, grants, and technologies. They find that such support helps to expand funding options such as crowdfunding and other peer to peer lending avenues. Malaga, Mamonov and Rosenblum (2018), Bapna and Ganco (2021) and Venturelli, Pedrazzoli, and Gallo (2020) document that ethnic and gender similarities between investors and entrepreneurs are a key driver for the amount invested in an equity crowdfunding campaign. These more recent findings indicate that minority businesses that can signal support and leverage crowds with similar characteristics my fare better with this non-traditional funding option.

Women-led ventures often start and are run with less capital than male led ventures (Robb, 2013[2]; Roomi et al., 2009; Shaw & Lam, 2010). Limited capital makes it more challenging to grow and scale business operations, impeding long term success. In addition, a 2023 World Economic Forum diversity, equity and inclusion report indicates that Black women founders received just 0.34% of total VC funding in 2021. Moreover, the report suggests that funding support for minority female businesses ebbs and flows with tragic event cycles[3]. This underscores the lack of structural support for minority-female led business ventures and the need for funding alternatives. A better understanding of how success rates have fared in more recent years and the characteristics that may drive successful funding campaigns is of significant interest for all the aforementioned reasons.

Hypothesis Testing

This analysis tests 3 hypotheses.

H1: Minority entrepreneurs raise less capital than non-minority entrepreneurs via crowdfunding campaigns.

H2: Female entrepreneurs raise less capital than male entrepreneurs via crowdfunding campaigns.

H3: Minority female entrepreneurs raise less capital than a) minority male b) female non-minority entrepreneurs.

Hypothesis 1 considers whether crowdfunding campaigns, which democratize funding decisions, provide minority founders with similar funding levels as non-minority entrepreneurs.

Hypotheses 2 and 3 examine crowdfunding capital raise levels for female entrepreneurs. Hypothesis 2 examines results for the overall female population relative to that of males, while Hypothesis 3 presents findings for minority-female led campaigns. We also examine potential entrepreneur characteristics that may mitigate asymmetric information between investor and founder, thus increasing odds of campaign success.

Signaling Theory Framework

To further interpret the dynamics of minority and female entrepreneurs’ access to crowdfunding capital, we draw on signaling theory framework which suggests that venture founders can reduce information asymmetry by conveying credible signals of quality to potential investors (i.e., founder professional background, educational background, or previous entrepreneurial success, etc.). In the context of crowdfunding, where investors often have limited direct information, such signals become especially crucial. Prior research in equity crowdfunding finds that investors respond to these signals: for example, campaigns led by experienced teams at larger firms are more likely to attract funding, as investors infer greater credibility and potential for success.

Ahlers et al. (2015) demonstrate that providing extensive financial information and risk disclosures, and founders retaining equity serve as positive signals that improve crowdfunding success rates. Conversely, the absence of strong signals can deter investment. In the case of underrepresented founders, signaling theory raises the question of whether minority and female entrepreneurs possess or can communicate the same quality cues as their non-minority male counterparts. Further, social role theory explores how those signals might be interpreted. If women and minority founders have fewer traditional signals (such as prior entrepreneurial successes, large personal equity contributions, or elite education credentials), or if their ventures are in industries perceived as low-growth, they may be at a signaling disadvantage.

The remainder of the paper is organized as follows: data, results, and conclusion.

Data and Methodology

The data from this study are collected from Kingscrowd, a data provider and service platform for crowdfunding investors and entrepreneurs seeking peer to peer funding. Once a Reg CF raise is registered with the SEC and has gone live on a crowdfunding platform, Kingscrowd collects the total amount raised, the total number of investors and other raise data. Kingscrowd accesses the primary campaign platforms public or private APIs to obtain raise information. When an API is not available, Kingscrowd uses automated web scraping or manual data collection. Their data collection began in 2016, however data collection and availability of some campaign characteristics were limited until 2020. This includes data on whether the capital raise has a minority founder. As such, while some of our tables cover the entire sample period of 2016-2023, our main analysis examines the impact of minority status and gender using data between 2020-2023.

For hypothesis testing, we first utilize a t-test to compare the difference in means, and a Wald test to compare the difference in medians between the capital raised by minority and female founders, respectively. We further test the hypotheses in a multivariate regression framework while controlling firm specific factors, industry and location fixed effects.

Descriptive Statistics

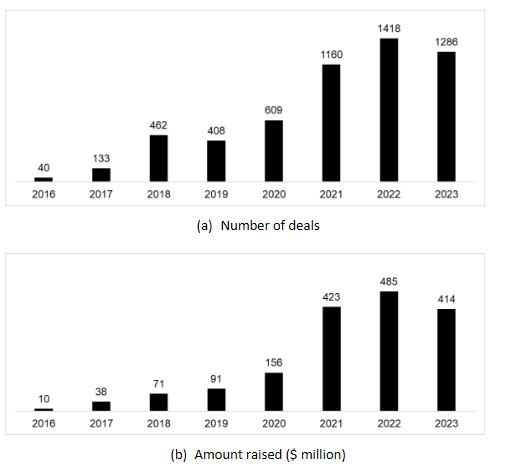

Figure 1 presents the number of Reg CF campaigns between 2016 and 2023. Figure 1a. shows a steady increase in the number of campaigns over time, with 2019 and 2023 being the exception. In 2019 the number of campaigns decreased by 11.6%, and decreased by 9.3% in 2023 relative to their previous funding years. Figure 1b. shows the amount of dollars raised (in millions) via Reg CF campaigns reported over the same period. The amount raised via Reg CF campaigns consistently increased over this time period, with 2021 realizing a 171% increase over 2020 dollars raised. The year 2023 is the exception in this trend, as 2023 saw a 14.6% decrease in dollars raised relative to 2022. The lower dollar amount raised may be in line with the corresponding decrease in the number of campaigns in 2023.

_and_amount_raised_(b)_via_regcf_over_time_(2016-2023).png)

Table 1 provides descriptive statistics for the overall sample. Of the 5,516 campaigns, the amount raised, on average, per campaign, is $305,833. These campaigns have an average target raise amount of $58,650. The variable ‘meeting target dummy’ average implies that roughly 74% of all campaigns met their minimum raise amount. This is an important statistic because a campaign must, at minimum, meet a minimum raise amount for the campaign to be deemed ‘successful’. A campaign that does not meet this minimum will require a founder to refund all funders. Descriptive statistics also show that founders averaged slightly greater than 8 years of relevant industry experience, and that these campaigns attracted roughly 366 contributing investors.

Gender and Racial Gaps of Crowdfunding Campaigns

Table 2, Panel A presents campaign statistics by gender (male vs female), and Panel B presents campaign statistics by minority/non-minority founder status.

Panel A shows that male led campaigns outpaced female led campaigns over 2 to 1. There were 3,285 male led, and 1,502 female led campaigns. Moreover, male campaigns raised $380,989, while female led campaigns raised, on average, $250,563. The difference is statistically significant at 1% level. The data also indicate that women led campaigns over our sample period tend to set significantly lower minimum raise amounts. Male led campaigns had an average minimum raise amount of $62,283, while female led campaigns had an average minimum campaign raise amount of $49,141. The difference is also statistically significant at 1% level. In addition, male founders attract significantly more investors (419) than their female counterparts (307) and had roughly 1 year of additional industry experience.

Panel B shows the data for minority or non-minority led campaigns, where minority is defined as of African descent, Asian, Hispanic, Native American, or Pacific Islander. There were a total of 2,775 non-minority founded campaigns, and 1,416 minority founded campaigns in our sample. Non-minority campaigns averaged $379,059 in funding, while minority led campaigns raised, on average, $292,175. Non-minority founder led campaigns also had significantly higher minimum target amounts, averaging $62,587, relative to minority founder led campaigns, which averaged $52,481. Minority founders, on average, attracted slightly more investors (362) than non-minority campaigns (353), and had fewer years of experience (6.79 years) relatively to non-minority founders (8.55 years).

Overall, findings from Table 2 support hypothesis 1, signifying a racial funding gap and hypothesis 2 which corresponds to a gender funding gap in crowdfunding campaigns.

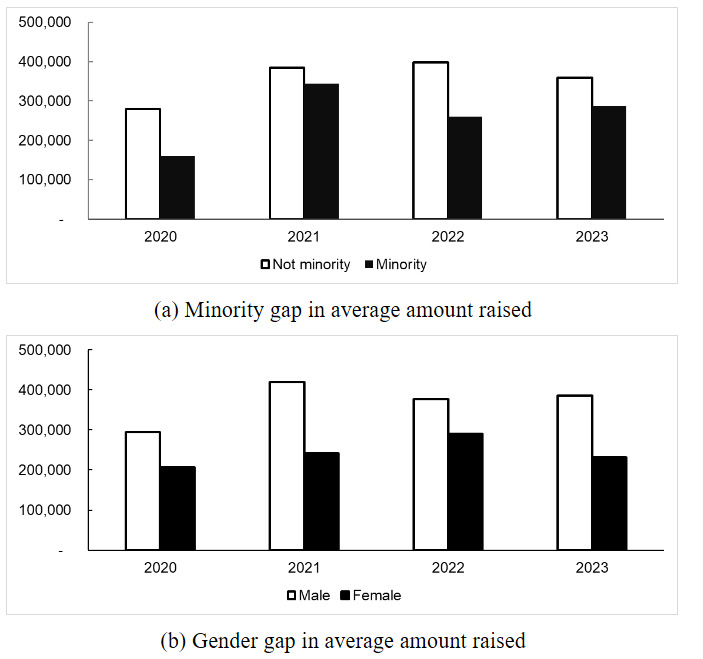

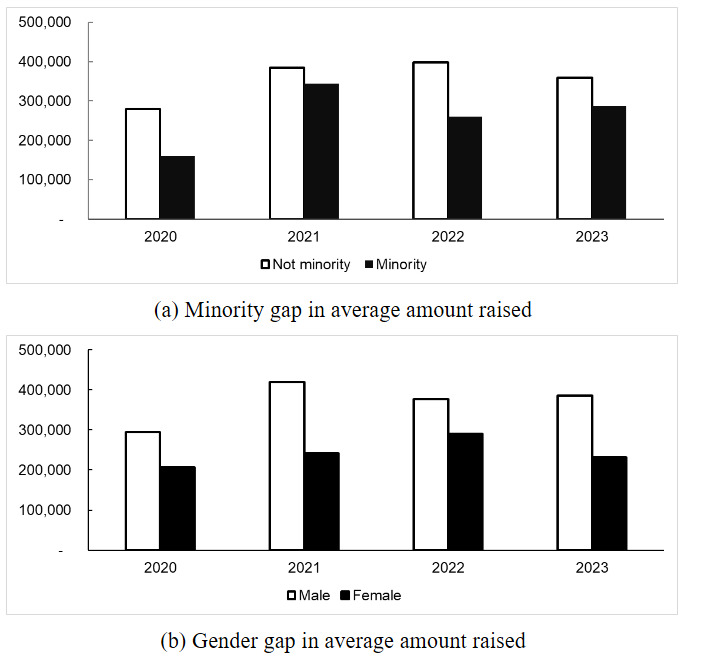

Figure 2 illustrates, graphically, the average amount of capital raised by minority status (Figure 2a), and gender (Figure 2b) between 2020-2023. Figure 2a shows that non-minority founders raised more capital than minority founders, and consistently so, over our sample period. The Figure also shows that this gap narrowed significantly in 2021. This decrease is likely the result of an outpouring and pledge of financial support by corporations and organizations, nationwide, in support of Black and minority community and business. This support came largely on the heels of the highly publicized killing of George Perry Floyd, Jr., a Black man, at the hands of a White police office in May of 2020[4]. Figure 2b shows male led campaigns raise more capital than female led campaigns, providing support for Hypothesis 2.

Figure 2a and Figure 2b, collectively, show that, on average, non-minority and male founder led campaigns consistently earn more capital relative to minority and female founder led campaigns.

Table 3 tests the significance of the aforementioned racial and gender campaign funding gaps, in means and in medians to provide further robustness. We use the t-test to compare the difference in means and the Wald test to compare the difference in medians. Panel A, which tests H1, or whether there is a significant racial funding gap in the capital raised via a crowdfunding campaign, shows that non-minority founders raise, on average, $86,883 more than minority founders. The median difference was $21,277. Both differences are significant at the 1% level, which indicates the presence of a statistically meaningful minority capital raise gap in crowdfunding campaigns over our sample period.

Panel B presents the results for H2 and indicates whether there is a significant gender funding gap in the amount of funds raised by male and female founders. Results indicate, on average, that men raise $130,426 more than women, with a median difference of $41,851. Both differences are statistically significant at the 1% level, which would indicate the presence of a crowdfunding gender funding gap. When comparing Panels A and B from Table 3, we also note that the racial funding gap is smaller than the gender funding gap. This may indicate that gender, more so than minority status, plays a significant role in the amount of funding received via crowdfunding relative to male and non-minority founders.

By contrast, a report by McKinsey & Company indicates that, in 2022, Black and Latino founders received 1, and 1.5%, respectively, of all US VC funding[5], while women received 1.9% of all funding. While this statistic, on the surface, may indicate that women founders receive higher funding levels via VC, all aforementioned percentages are infinitesimal compared to overall funding levels. Harvard’s report on Advancing Gender Equity in Venture Capital states that the 30-year average of the amount of funding that women receive from VC is 2.4%. This statistic has gained little ground when comparing it to the 2.3% of VC funding women received in 2018[6]. Further, these numbers are even more dire for Black and Latino women founders, who received 0.1 percent of VC funds in 2022.

The above underscores the critical need to assess alternative sources of capital for minority and female founders. Thus far, while we find that funding gaps do exist, there appears to be significant improvement in accessing capital for minority and women founders, relative to VC funding statistics.

In addition to examining potential minority and gender funding gaps, we want to know how minority-female founders fare relative to minority-male, and non-minority female founders. These results are presented in Table 4. Using the same t and Wald tests to account for differences in means and medians, respectively, we examine whether minority-female founders 1) raise less than minority-male founders and 2) raise less than female, non-minority founders in aggregate (over entire sample period) and on average via crowdfunding campaigns.

Table 4 reveals differences between subgroups, highlighting disparities in funding outcomes. Minority female founders raised, on average, roughly $100,000 less than minority-male founders. This difference is significant at the 5% level. The difference in median amount raised is -$38,703, significant at the 1% level. Therefore, minority female founders raised significantly less than minority male founders. An important finding arises when comparing minority and non-minority female raise amounts. We find no statistical difference in the average amount raised between these two categories. However, the difference in median is -$18,375 and significant at the 5% level. The insignificant difference in means is likely the result of large campaign funding deals by minority female founders relative to non-minority female deal size. This represents a key finding. We have already identified that gender may play a greater role than minority status in terms of differences in funding levels. Further, this result may indicate that minority females are indeed able to attract and secure large funding levels relative to their non-minority counterparts. This is a favorable finding given the dismal VC funding numbers previously reported for segments of the minority female founder population. Minority female founders raised less than nonminority female founders, but the difference is more pronounced in median amounts. These results provide mixed evidence for Hypothesis 3. Overall, the findings suggest that gender may play a larger role than the intersection of race and gender when comparing funding rates for women.

Despite the general findings of gender and racial funding gaps in crowdfunding campaigns, this analysis presents promising finding for minority and female founders relative to funding gaps in VC. While non-minority founders raised $929 million over our sample period, minority founders raised $372 million, or about 28% of the total amount raised. Male founders raised about $1,098 million relative to female founders who raised $330 million, or 23% of the total. When the founders are either female or minority, the aggregate amount reached $591 million, in contrast to the $741 million raised by White male founders. In sum, these finding shows that minority and female founders receive over 44% of crowdfunding campaign investment, representing an undeniable increase in funding rates relative to VC investment. This improved funding rate presents a significant finding for minority and female founders who are seeking much needed capital.

Goal Setting and Investor Reach of Crowdfunding Campaigns

Thus far our findings indicate that non-minority males raise significantly more funding than minority-male, minority-female, and non-minority female founders seeking capital via a crowdfunding campaign. Moreover, we find that the funding gap between minority and non-minority female founders is insignificant over our sample period, which is promising in that race may play a less significant role in funding for women seeking capital via crowdfunding. Further, we want to know whether minority, female, and non-minority founders attract similar amounts of campaign investors, as it could be argued that crowdfunding campaigns attracting more investors may explain or contribute to higher funding amounts. In addition, we test whether these founders set similar minimum target raise amounts. Table 5 presents these results.

Panel A of Tabel 5 indicates whether minorities, on average, set similar minimum raise amounts as their non-minority counterparts. In order for a crowdfunding campaign to be deemed successful, the campaign must raise, at least, the minimum set target raise amount otherwise, the campaign is deemed unsuccessful and all capital is returned to investors. In this case the founder does not receive any capital. Panel A shows us that, on average, the minimum target raise amount for minorities is $52,481, roughly $10,000 less than the minimum target raise amount set by their non-minority counterparts. This difference is statistically significant at the 5% level. Accordingly, female founders set minimum raise amounts, on average, of $49,141, roughly $13,000 less than their male counterparts. This difference is statistically significant at the 1% level.

Panel B of Table 5 provides differences in mean for the number of contributing investors for campaigns run by minority and non-minority founders, as well as those for male vs female led campaigns. We find that non-minority founders do not attract significantly more campaign investors. We show a difference in means of 9 investors, where minority investors attracted 9 more investors over our sample period than their non-minority counterparts. This finding is in line with Cumming, Meoli, and Vismara (2021) who indicate that minority entrepreneurs tend to attract more investors. Moreover, our findings indicate that this difference is not statistically significant. This may show, at least in part, that provide further evidence that race may be less of a factor in crowdfunding, and in terms of attracting investors in crowdfunding campaigns for minorities. By contrast, the data show that males attract, on average, 419 investors, while females attract 307 investors. This is a difference of 112 investors, on average, per campaign, and this difference is statistically significant at the 1% level.

Table 5 shows us that minorities tend to set significantly lower minimum target raise amounts, yet attract similar number of investors, relative to their non-minority counterparts. Moreover, females also tend to set lower minimum target raise amounts and tend to attract significantly fewer campaign investors.

Multivariate Analysis of Entrepreneur and Firm Characteristics

We extend the univariate analysis to perform multivariate regressions of entrepreneur characteristics and crowdfunding success factors. The dependent variable in both models is the natural logarithm of the amount raised during crowdfunding campaigns. Model 1 includes a dummy variable for gender, where “female” equals 1 for female founders and 0 for male founders. Model 2 incorporates a dummy variable for minority status, where “minority” equals 1 for minority founders and 0 for non-minority founders. Other explanatory variables include the number of investors, market type (wide vs. niche), log-transformed revenue, log-transformed total assets, and founder years of industry experience. The models control for industry and state fixed effects to account for unobserved heterogeneity across sectors and locations.

Table 6 presents the results of the multivariate regression analysis of crowdfunding success factors. In Model 1, the coefficient for the female dummy is -0.3084 and significant at the 1% level, indicating that campaigns led by female founders raise approximately 30.84% less (in log terms) than those led by male founders, holding other factors constant. In Model 2, the coefficient for the minority dummy is -0.2535 and significant at the 1% level, suggesting campaigns led by minority founders raise approximately 25.35% less (in log terms) than those led by nonminority founders. In Model 3, the coefficient for the minority female dummy is -0.4045 and significant at the 1% level, suggesting campaigns led by minority female founders raise approximately 40.45% less (in log terms) relative to other founders. These results support Hypothesis 1, 2, and 3.

Most of the control variables are statistically significant as well. The number of investors positively affects the amount raised in all three models, with a coefficient of 0.0008, significant at the 1% level. This indicates that an increase in the number of investors marginally increases the crowdfunding amount. The market type variable (wide = 0 vs. niche = 1) is positive in all three models but is not statistically significant. The log of revenue shows a negative association with the amount raised in all three models, with coefficients of -0.0145 (Model 1), -0.0163 (Model 2), and -0.0157 (Model 3), respectively. This effect is significant at the 5% level in Model 1 and at the 1% level in Models 2 and 3. The negative relationship between revenue and the amount raised in crowdfunding might seem counterintuitive. One possible explanation is that companies with higher revenues may appear less “in need” and thus may attract less investment.

The years of industry experience of founders positively impact the amount raised, with coefficients of 0.0112 (Model 1), 0.0103 (Model 2), and 0.0108 (Model 3), all significant at the 5% level. The log of total assets has a strong positive association with the amount raised, with coefficients of 0.0904 (Model 1), 0.0941 (Model 2), and 0.0924 (Model 3), all significant at the 1% level. All three models explain approximately 29% of the variation in the crowdfunding amount.

The analysis highlights that demographic factors, such as gender and minority status, alongside company-specific factors such as assets and founder experience, significantly influence crowdfunding outcomes. Female and minority founders face notable disadvantages in raising funds, while greater total assets and founder industry experience enhance fundraising success.

Conclusion

This analysis examines whether crowdfunding offers female and minority founders greater access to entrepreneurial capital and characteristics that may contribute to campaign success. We document significant funding gaps in equity crowdfunding campaigns for both minority entrepreneurs and female entrepreneurs relative to non-minority, male entrepreneurs. Despite attracting a slightly greater number of investors, minority-led campaigns raise on average $292,175, or about 23% less than the average of $379,059 raised by non-minority founders, underscoring that funding amounts per investor tend to be smaller for minority-led campaigns. Moreover, female founders face challenges in attracting similar numbers of investors relative to males and raise, on average, 34% less capital than their male counterparts. Minority and female founders, on average, have fewer company assets which may contribute to lower funding rates however, therein lies the paradox. These founders start from a disadvantaged place given limited funding opportunities at start-up phase, limiting growth, thus perpetuating the funding gap cycle.

Our findings indicate that gender bias may be stronger than minority bias in equity crowdfunding when comparing the number of participating investors and overall funding gap levels. This result provides some preliminary evidence that equity crowdfunding may present less bias in terms of race than funding avenues such as venture capital (VC) where minority funding levels are historically infinitesimal.

Minority female entrepreneurs face compounded challenges at the intersection of race and gender. As such, we examine how minority female founders fare relative to minority male and non-minority female in terms of investor participation and raise levels. We document that minority female founders raise less capital than minority males, however, we did not find a statistically significant difference in the average amount raised by minority and non-minority female founders. This finding provides additional preliminary evidence that gender may play a greater role than race in equity crowdfunding, and suggests that minorities, and in particular minority females, may find a more receptive investor audience by pursuing equity crowdfunding relative to VC.

Identifying and acknowledging the systemic disparities in our funding systems is critical if we are to ensure equity for founders who desire to start, sustain, and grow their business. The disparities highlighted underscore the need for targeted interventions to close the racial and gender funding gap and foster equitable economic opportunities. Minority and female founders initiating crowdfunding campaigns will benefit from sending credible signals (experience, entrepreneurial traction, endorsements), mobilizing identity-aligned communities, and crafting pitches that balance confidence and deep business acumen and skillsets. Equipping investors with the funding gap awareness of social role bias may also assist in addressing funding disparities. Strategies such as standardized investor questioning and formats that are grounded in business facts may be advantageous.

Traditional funding avenues, long characterized by inequities, are mirrored in crowdfunding platforms, though the latter offers some potential for democratizing access to capital. On a positive note, our results indicate that women and minority founders have significantly better funding odds pursuing crowdfunding campaign than woman and minority founders seeking funds via VC. However, while crowdfunding offers promise as an alternative to traditional funding, structural inequities remain an obstacle. The data call for a more nuanced understanding of investor behavior, campaign strategies, and platform dynamics to better support minority and female entrepreneurs. Tailored policies and practices, such as targeted funding programs and bias-reduction measures, are essential to bridge these funding gaps and realize the full potential of diverse entrepreneurial contributions to the economy.

https://advocacy.sba.gov/wp-content/uploads/2021/08/Small-Business-Facts-Business-Owner-Wealth.pdf

https://advocacy.sba.gov/wp-content/uploads/2019/05/rs403tot2.pdf

The articles here provide context around the media attention given to the financial support of Black and minority communities and business.

https://www.cnn.com/2021/05/25/business/corporate-america-anti-racism-spending/index.html

https://www.hks.harvard.edu/centers/wappp/research/past/venture-capital-entrepreneurship