INTRODUCTION

Growth is a very important strategic goal for both family and non-family firms (Miller & Le Breton-Miller, 2006). However, due to family firms’ peculiarities and the overlap of their three different systems (family, management, and ownership), their reasons for growth can differ from those of non-family firms. Several researchers in this area (e.g. López-Cózar-Navarro et al., 2017) have noted that family firms’ motivations for growth can differ from those of non-family firms, since both ownership and family ties influence on the firms’ strategic objectives (Theodorakioglou & Wright, 2000). Therefore, De Massis, Kotlar, et al. (2018) indicate the need for a better understanding of the mechanisms through which economic and non-economic sets of preferences shape family firm behaviour.

The desire to grow is determined by the motivations or intentions of the entrepreneur (Dutta & Thornhill, 2008). In the specific case of family businesses, De Massis, Kotlar, et al. (2018) indicate the relevance of these intentions in the setting of strategic objectives for the company and refer to them as the will, the favourable family disposition, to perform a distinctive behaviour. Therefore, the role of the family as a predecessor for setting goals in family businesses is relevant (Williams et al., 2018).

A company’s degree of familiness could influence its pursuit of growth. This degree of familiness results from the family’s close identification with the firm and its attachment and commitment to the company (Denicolai et al., 2019). While both family and non-family firms consider that this growth can be motivated by economic and strategic reasons, the person who runs the business could cite family reasons as the basis for the family firm’s search for growth. Therefore, in this particular case, attaining business growth and/or survival has a more purposeful meaning than in a non-family business.

In generational handovers, when the number of family members who join the firm increases, the business will need to grow, to ensure that the size of the legacy received by each member of the succeeding generation does not diminish. In this way, the family members have similar business motivations and interests as founders or predecessors. Alternatively, the firm could handle the family complexity by pruning the family tree (Lambrecht & Lievens, 2008).

On the other hand, ensuring business survival could become the only alternative to handing the firm over to the next generations. Therefore, several researchers (e.g. Zahra, 2003) have considered generational change or desire for continuity through succeeding family generations as a variable for distinguishing family from non-family businesses.

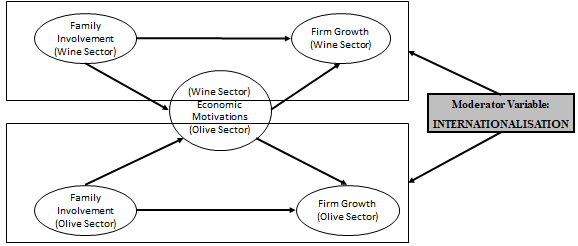

This study analyses whether the family influences business objectives, specifically, the firm’s growth. Additionally, it studies the impact of economic factors on the relationship between family involvement and firm growth. The family’s influence on business objectives could become an intangible business resource, specifically, as a driver of business growth and survival. This intangible resource is understood as the outcome of family involvement in the business (Denicolai et al., 2019) that either limits or facilitates the achievement of non-economic objectives (Cabrera-Suárez & Olivares-Mesa, 2012). Furthermore, family involvement has been commonly used as a variable for identifying the family’s power in shaping a firm’s goals, strategies, and behaviours (Deephouse & Jaskiewicz, 2013).

Although firms can choose from different strategies for their survival and growth, the way in which the divergent preferences of business owners (motivations) influence business internationalisation arouses the interest of numerous authors (Braga et al., 2017; Singla et al., 2017). Even so, certain elements remain to be addressed when identifying the reasons why family businesses (FBs) go international (Alkaabi & Dixon, 2014). In this way, various strategic and/or economic motivations can justify business internationalisation, although, in the case of family businesses, other motivations related to the family itself may be present. This study analyses the role economic motivations play in business growth from an international strategy and how family involvement is related to the selection of this strategy. Several authors as Alayo et al. (2019) consider internationalisation as an important entrepreneurial strategy for long-term growth and survival. The development of this strategy increases the performance of FBs by facilitating their survival and increasing their sales (Heileman & Pett, 2018).

The literature has acknowledged that family firms differ from non-family firms in attitudes and behaviours when internationalising (e.g., Heileman & Pett, 2018). This study goes further, to address the need of investigating possible differences between companies, not only depending on their family character, but by considering the heterogeneity of FBs, with varying degrees of family influence in the business, and targeting companies with and without an international strategy (Heileman & Pett, 2018).

Focusing on economic motivations, a company that grows in markets where costs can be reduced and greater margins and/or market shares can be obtained can increase the value of the company and, therefore, the wealth of its owners, generating profits, increasing sales, improving results and increasing the performance of the company (Banalieva & Eddleston, 2011). This can be of utmost importance to ensuring the growth and continuity of a family business, where the achievement of economic and non-economic objectives is closely related to the decisions made by FBs about their conduct in international markets (Gómez-Mejia et al., 2010).

The target population we have chosen for this study comprises firms belonging to two Spanish industries in which internalisation is particularly relevant— the olive oil and wine sectors. To achieve our research goals, we conducted quantitative research based on the partial least squares (PLS) methodology, which offers a wide range of possibilities for management research.

The results show a remarkable role of the economic motivations in explaining the link between family involvement and the desire to grow. The higher the family involvement, the lower the importance of economic motivations and the desire to grow which, at least, does not happen from the development of an internationalisation strategy.

Following this introduction, this paper is structured into four sections. In the following sections, a review of the literature covers potential reasons for FBs’ pursuit of growth and the current approaches to analysing their internationalisation strategy as an effective means to achieve growth. A description of the empirical study is presented, followed by the study results. The discussion and main conclusions are described, followed by the study’s main limitations and recommendations for future research in this area.

LITERATURE REVIEW

In today’s changing global competitive environment, business growth has become a central topic in the study of strategic management. Revenue generation, value addition, and increased business volume are considered crucial elements in defining business growth (Gupta et al., 2013). Indeed, business goals commonly include firm survival, profit, and growth.

While some researchers (Donaldson & Lorsch, 1984) have noted that firms consider growth as a way to ensure long-term continuity, others (Goold, 1999) have considered growth to enhance executives’ reputations or to acquire the most qualified employees for high-level positions. Canals (2001) identifies other reasons for pursuing growth, such as finding and maintaining the most talented staff, attracting investment capital, and dealing with risks related to a new superior product’s launch, and risks from working in a mature sector.

Reasons for family businesses’ pursuit of growth

The relationship between family ownership and business growth is complex (Bjuggrena et al., 2013). Some studies show that FBs are usually characterised by a lack of or lower growth rate, compared to non-family businesses (Machek, 2015). Ward (1997) alludes to some of the reasons that explain the above, such as financial problems arising from business and family, their presence in mature markets, resistance to change or lack of flexibility, conflicts of succession and incorporation of new generations and the lack of unanimity in values, objectives and needs of the family. While Calabrò et al. (2017) conclude how the family character of the company can favor growth when the group of owners is neither too small nor too wide and, in addition, there is a high family identity towards the company. Along these lines, Chen et al. (2014) argue that at certain times when the desired growth is achieved, non-economic motivations (such as increasing employment generation) can prevail over economic ones (such as achieving higher sales volume); however, at other times when such growth is not achieved, economic motivations can take centre stage.

The desire of growth of the family business comes when the family grows, so does the business, understanding that a family who wants to transfer a legacy to the next generations should follow a growth-oriented strategy. Some studies have focused on the pace of growth of the family and business (e.g., Bañegil Palacios et al., 2013). Other explanations for FBs’ pursuit of growth are related to their significant human resource concerns and higher employee commitment (Ahluwalia et al., 2017). A family firm that is not growing finds it very difficult to attract or promote managers who can provide the firm new knowledge and who can help to promote an entrepreneurial spirit within the firm. These businesses represent a source of employment generation for family members (Castillo & Wakefield, 2007; Theodorakioglou & Wright, 2000), both current and future (Bañegil Palacios et al., 2013). However, if the company does not grow there will be a lower possibility of offering jobs positions for family members who wish to join the business and have no place in the existing structure.

This literature review shows that owing to their distinct characteristics, family firms have motivations for growth that differ from those of non-family firms. Like in non-family firms, we find economic motivations for growth in FBs, as well as strategic reasons. Both types are considered obvious reasons for the desire of firms to grow. However, other strategic and family reasons appear to be more relevant than economic reasons in driving family business’ growth, since FBs often develop behaviors that are not justified by economic rationale (Stieg et al., 2018). Hence:

Hypothesis 1. Economic motivations mediate the relationship between family involvement and firm growth in both the wine and olive sectors.

Internationalisation as a growth-oriented strategy for family businesses

Successful operations in international markets may be critical to the growth objective of many businesses, especially family firms (Heileman & Pett, 2018). Internationalisation is a strategy that can guarantee growth (Hynes, 2010). An internationalisation strategy allows a company to exploit its ownership resources to achieve a competitive advantage abroad. At the same time, the development of this strategy per se allows the company to increase resources, to boost its profits in the domestic market, which in turn moves its internationalisation strategy forwards. Thus, international business expansion as a growth-oriented strategy implies improving and/or maintaining the competitive market position.

In this area of research, Sciascia et al. (2013) highlight that a 100% family involvement in the board of directors may produce negative effects that may reduce the firm’s capability to internationalise, since exclusive family involvement may constrain board capital by limiting human and external social capital.

Gómez-Mejia et al. (2011) note that some small FBs prefer not to internationalise since doing so could dilute ownership (by needing a greater volume of capitalisation) and decrease the family’s power. However, it should be noted that non-family members’ involvement in FBs could also influence performance and growth (Farrington et al., 2011).

In the same area of research, Kraus et al. (2016) conclude that despite the importance of external resources (external ownership, a non-family CEO, non-family members on the advisory board, and international networks) in family firms’ internationalisation, their owners face a constant trade-off between benefiting from external resources and jeopardising their socioemotional wealth endowment. Therefore, family companies show limitations in their resources and capabilities to achieve performance and link internationalisation with the endangering of family firm’s socioemotional wealth (Moreno Menéndez et al., 2021; Stieg et al., 2018), the fear of deterioration of this intangible asset sometimes leads family companies to give up the development of important business strategies (Mahto et al., 2018).

Thus, FBs’ ownership and management structures seem to influence significantly their international expansion, which implies that a significant family presence in both would not lead to growth through an internationalisation strategy. In contrast, a lower level of family involvement would push FBs in the opposite direction. To summarise:

Hypothesis 2. In both sectors, an internationalisation strategy moderates the relationship between family involvement and firm growth

METHODOLOGY

Participants

The study sample comprises of Spanish wine and olive oil production companies, including both family and non-family businesses. We define the study sample based on available secondary information, namely the database of companies in both industries maintained by the Spanish Ministry of Agriculture, Food and Environment, and the databases of the Regulatory Boards of the most representative Designations of Origin in the Spanish wine and olive oil industries. When determining which wine and olive oil production firms to include in the study sample, we also use the information in the SABI (Sistema de Análisis de Balances Ibéricos), a database of accounting data from Spanish firms.

The final sample comprises 418 firms (family and non-family firms), of which 257 firms are from the wine industry and 161 firms are from the olive oil industry. The data from the survey were collected from September 2016 to March 2017. The response rate was 10.70%. The data were collected by telephone (i.e. the respondents were asked survey questions over the telephone) and by e-mail, (i.e. a link to the online questionnaire was emailed to the participants).

Measurements

The information collection instrument is developed based on Churchill and Surprenant’s (1982) methodology for measurement scale construction. First, each study construct is defined and all the potential dimensions are extracted from the literature reviewed. The items obtained are complemented with in-depth interviews with academics and wine and olive oil industry experts. A pilot test to validate the questionnaire is conducted with managers of wineries and olive oil mills, and senior representatives of the Regulatory Boards of Designations of Origin and of associations and foundations in the wine and olive oil industries. A pre-test is conducted among industry experts, and the questionnaire is revised by excluding redundant or unclear items.

The questionnaire includes three sections of items. The first identifies the degree of family involvement in ownership and management, with the aim of determining how family involvement influences the firm growth objective. The second analyses the types of reasons for the pursuit of business growth and survival. Finally, the third obtains information about the internationalisation as a key strategy to achieve the objectives of growth and survival.

Family involvement is defined in terms of ownership and management. De Massis et al. (2012) highlight that an operational definition of a family firm is most frequently based on family involvement in ownership and management.

Thus, we understand family involvement in the business as a continuum variable, and we can find at the ends of the continuum:

-

Companies with a high level of family involvement, which executive management positions and ownership are entirely held by the family.

-

Companies without family involvement and therefore, could be considered as non-family businesses, which the family has neither ownership share nor management positions.

Economic motivations are measured using two items—increase in profits and in profitability—both of which have been previously considered in the study of family firms’ economic goals (e.g. De Massis, Kotlar, et al., 2018).

Meanwhile, desire for growth is measured using two items: a) the intention of making the business grow, and b) the intention to create future employment. In previous research, both these items have been considered valid measurements of businesses’ intention for growth (e.g. Cliff, 1998).

Finally, a company with an international strategy was classified as an international company. Previous studies have considered many variables to measure business internationalisation, of which one of the most deployed is export propensity (Fernández & Nieto, 2005), a dichotomous variable for whether the firm exports or not. In our study, exporting companies were considered as international and non-exporting companies as non-international.

Statistical analysis

We conduct quantitative research based on the PLS methodology, which offers a wide range of possibilities for management research. With regard to statistics in family firm research, SEM represents an advanced version of general linear modelling procedures (e.g. multiple regression analysis) (Astrachan et al., 2014).

Measurement of instrument validity

The assessment of the measurement model for reflective indicators in PLS is based on individual item reliability, construct reliability, convergent validity, and discriminant validity (Roldán & Sánchez-Franco, 2012). Individual item reliability is considered adequate in this study because all the indicators and dimensions have loadings above 0.676 (Table 1)[1]. All the constructs and dimensions meet the requisite construct reliability, as their composite reliabilities (CR) are greater than 0.7 (Table 1). To assess convergent validity, we examine the average variance extracted (AVE). All the latent variables have convergent validity, as their AVEs surpass 0.5 (Table 2).

Finally, Table 2 shows that all the constructs have discriminant validity, following both the Fornell-Larcker and the strictest HTMT.85 criteria (Hair et al., 2017). This means that all the constructs are empirically distinct.

RESULTS

In the structural model assessment, we estimate the path coefficients, their significance via bootstrap tests, the R2 values, and the Q2 tests for predictive relevance. This analysis is performed for both the total sample and the four subsamples in each sector the wine sector and the olive sector (see Figure 1). The Q2 value is obtained using the blindfolding procedure for a specified omission distance (in our case, 7). When a PLS path model exhibits predictive relevance, it accurately predicts data not used in the model estimation. Q2 values larger than zero for a specific reflective endogenous latent variable indicate the path models’ predictive relevance for a particular dependent construct. In our case, all the reflective constructs exceed zero, showing predictive relevance. The calculation of the standardised root mean square residual (SRMR) completes the goodness-of-fit analysis for the structural model. Henseler et al. (2014) advocate the use of the SRMR indicator to measure a model’s goodness of fit, recommending values of less than 0.08. For the structural model, the value is 0.06 for the wine sector and 0.05 for the olive sector.

In the main model, to test our mediation hypothesis (H1), we apply the analytical approach described by Nitzl et al. (2016). To establish a mediating effect, the indirect effect must be significant. Hence, in step 1, we determine the significance of the indirect effects. In step 2, we define the type of mediation. For full mediation, the direct effect must be insignificant. The results for the total, direct, and indirect effects are presented in Table 3.

The direct effect of family involvement (-0.015) on firm growth is significant [-0.265;-0.009], the indirect effect of economic motivations (-0.052) [-0.302,-0.003] is also significant. Thus, economic motivations partially mediate the relationship between family involvement and firm growth in both sectors. This finding illustrates the main role of economic motivations, and therefore, H1 is supported.

Firm internationalisation multi-group analysis (MGA) for moderation

The multi-group analysis (MGA) divides the sample into two groups and considers firm internationalisation as a moderating variable. To this end, the permutation test is mainly used (5,000 permutation runs; two-tailed 0.05 significance level) for each group of observations. Statistically significant differences in path coefficients between subsamples are interpreted as moderating effects (Qureshi & Compeau, 2009).

Therefore, we run two MGAs, one for each moderating variable, using a non-parametric approach (the bias-correct 95% confidence intervals). In this case, if the parameter estimate for a path relationship of one group (Table 3) falls outside of the corresponding confidence interval of another group (Table 3) and vice versa, no overlap exists and the group-specific path coefficients can be assumed to significantly differ (as indicated by the significance level α) (Sarstedt et al., 2011). The next step is to analyse the differences between coefficients in the different paths. If these differences are significant, the moderating variables have a moderating effect (see Table 3).

Based on the analysis results presented in Table 3, we conclude that firm internationalisation moderates the relationship between family involvement and firm growth, which is mediated by economic motivations in the wine sector. First, when there is no internationalisation, economic motivation has a full meditation effect on the relationship between family involvement and firm growth, but when there is internationalisation, economic motivation has only a partial effect.

However, in the olive sector, firm internationalisation does not moderate the relationship between family involvement and firm growth, which is partially mediated by economic motivations regardless of whether companies are internationalised or not. That is, the mediator role of economic motivations is the same in firms that are internationalised and those that are not internationalised. Thus, we can conclude that, depending on the sector, the internationalisation of the firm can play a moderator role.

DISCUSSION

The level of family involvement presented by the companies studied does not directly influence the desire for growth in those companies. This statement is consistent with the debate that is still open in the literature about the influence of the family on the growth of the family business (De Massis, Frattini, et al., 2018; Moreno-Menéndez & Casillas, 2021). Paying attention to the ownership business structure (i.e. family or nonfamily), Bjuggrena et al. (2013) note that family-owned firms seem to be characterised by lower growth rates than non-family firms.

This finding addresses the previous inconclusive research findings related to the influence of the family and non-family nature of a business on its growth (Goel et al., 2012). Previous research work indicates that growth can mean a higher level of risk and a loss of family control, so FBs prefer to develop growth in the long term and not in the short term (Moreno-Menéndez & Casillas, 2021). However, growth sometimes becomes necessary when the family perceives the danger of the loss of socioemotional wealth, which implies the need to open up to a strategic change, such as that caused by growth, for the achievement of the family’s long-term economic goals (Verbeke et al., 2020).

To this point, this work considers the heterogeneity of FBs as a continuous variable that influences business strategies (e.g. Sciascia et al., 2013), and that such heterogeneity implies dissimilar levels of family involvement in businesses (Berrone et al., 2012) that influence the perception of the company’s growth. In light of the above, the results achieved in this research work show how the role of economic motivations in the relationship between the family involvement shown in the company and its desire to grow is relevant. Thus, economic interests do partially explain this relationship, both for companies in the Spanish olive sector and for companies in the Spanish wine sector. Firms with greater family involvement the family could be highly dependent on the business in financial terms and shows a stronger fear to lose the control of the business, one of the main barriers to the internationalisation (Bose, 2016); therefore, such firms’ desire to grow is less than that of firms with lower family involvement, paying attention to economic interests. Goel et al. (2012) note the reasons for this lesser desire to grow. They state that growth often dilutes family control, so that families, whose social and familial interests are closely tied to the control of their firms’ economic future would have less incentive to grow quickly because to do so requires external sources of capital, which may imply a loss of control. Vincent Ponroy et al. (2019) gave another argument when the family business grows a loss of collective cohesion could exist and heartbreak in family-employees relationships.

Related to the above finding, a higher level of family involvement in the business leads to a lower importance of economic motivations in explaining the business’s desire to grow, and vice versa. We conclude that economic motivations, specifically, the increase of profitability and profit, influence family firm growth, considering the family involvement the company has.

Additionally, since an internationalisation strategy could be a pillar of business growth and survival (Prange & Verdier, 2011), we introduce such strategy as a moderating variable in our analysis of whether the previous research findings are maintained when the firms are international and when they are not.

For companies in the olive oil sector, internationalisation does not reveal any new understandings. Both for internationalised olive companies and for those that do not develop an international strategy, economic motivations partially explain the relationship between the level of family involvement present in the company and the desire to grow. Undoubtedly, in FBs in the Spanish olive sector, previously analysed by studies such as Gómez-Mejía et al. (2007), risky decisions, such as growing the business by entering into new markets, are avoided unless the danger posed to these companies by the loss of their socioemotional wealth is perceived, where increasing their performance to avoid risk is a priority. This is also observed in non-internationalised wine companies, where economic interests partially explain the relationship between family involvement and business growth. In this way, in companies without an internationalisation strategy, when the level of family involvement is very high, the economic motivations are almost irrelevant to explaining the desire to grow. The role of the economic motivations to explain the link between family involvement and desire to grow is remarkable. The higher the family involvement, the lower the importance of economic motivations and the desire to grow which, at least, does not happen from the development of an internationalisation strategy. Thus, in these companies, interests other than purely economic ones such as family and/or strategic motivations, could have a greater weight in the search for international growth, a result consistent with those previously obtained by authors such as Kotlar and De Massis (2013). They point out the priority of achieving family objectives as a result of the interaction between family members, as opposed to the achievement of economic objectives that arises as a result of professional interaction, when professional managers and external shareholders are present.

Internationalisation adds useful information for explaining the relationship between family involvement in the business and the firm’s growth orientation. In non-international firms, the higher the family involvement in the business, the lesser the family business’s desire to grow, and this relationship is explained by the low economic motivation to grow in companies from both the olive oil and wine sectors. Only, in international wineries, there is a clear relationship between family involvement and desire to grow, explained by economic interests. Firms with lower levels of family involvement have a greater desire to grow internationally to increase profitability.

In summary, despite the importance of economic motivations in the pursuit of business growth, other types of motivations can also explain these firms’ desire for growth. This statement is consistent with Zaefarian et al.'s (2016) findings considering international firm growth. They highlight that family firms, after making their first entry into international markets, pursue international opportunities more purposefully to create opportunities for growth and increase longevity for the next family generations, during which motivations other than economic ones have a greater weight.

Our findings are also explained by the results of previous works such as that by Alayo et al. (2019) that indicate that a greater involvement of the family in the business, understood by relatives of multiple generations in senior management positions, adds complexity to the management and hinders the business process in international markets. In turn, the internationalisation strategy requires greater planning and coordination than other strategies, because of its complexity (Pacheco, 2019) that, in addition, may require external financing, which would mean reducing the family’s independence in business management so that economic motivations do not compensate for the difficulties that internationalisation strategy can entail. The fear of losing family assets implies that the family wishes to maintain control of the business and avoid taking risks (López-Cózar-Navarro et al., 2017). Thus, a greater degree of family involvement may explain a lower orientation to growth due to economic motivations, due to the desire to preserve socioemotional heritage, motivation that do not favor growth opportunities based on an internationalisation strategy.

Implications

Previous findings have implications for academics who are interested in getting the family involvement threshold at which FBs would want to develop and implement growth-oriented strategies, such as the internationalisation one. Additionally, the owners and executives of family firms who want to identify growth-oriented actions will have to cede some of the business control to non-family members. This result suggests that family commitment to the business operations and management, which family members share with people outside the family, can boost the internationalisation strategy as a growth-oriented strategy and its chances of success. Also increasing the family business’s professionalism is essential for increasing its market exploration capabilities (Yeniaras et al., 2017) (e.g. in the international market). Thus, Penco et al. (2020) alludes to the complexity of the international strategy that requires planning to be well-prepared and shared by external managers whose presence reinforces even more the organization’s commitment to that strategy.

Differently, our findings can help executives of FBs who show a high level of family involvement to consider the need for growth and the relevance of economic motivations to achieving that objective. In fact, there is a situation in business families where, in response to the business, there are limits to growth plans. However, value maximisation should be important as well becoming an objective in family firms as it is in non-family firms.

On the one hand, family businesses’ managers should work with long-term objectives, what implies developing projects without pressure for having to obtain short-term outcomes or profitability in the market (Vincent Ponroy et al., 2019). Otherwise, they have to consider that improving profitability or profit helps a business grow, addressing how internationalisation favors firm performance (Pacheco, 2019), and therefore, improves the business’s competitive position in a more globalised, dynamic, and complex environment, which influences business performance.

Our results could help businesses achieve long-term survival, and therefore, the possibility of handing the business over to the next family generation. This objective is motivated not only by economic reasons but also by non-economic reasons, which may be more relevant in these firms, since achieving this objective could become a way to maintain the nature of the family firm. In the search for growth, family managers should be very motivated by the development of strategic options, such as internationalisation, to increase the probability of success (Andersson, 2000).

Limitations and Future Research Directions

Some limitations of this article lead towards future research directions. First, other concepts make up the constructs of economic motivations and firm growth, and thus, future research should consider other possible dimensions for creating those constructs. Second, this work focuses on the study of the relevance of economic motivations in attempts to grow the company as it relates to the development of an international strategy or the lack thereof. Thus, on the one hand, it is necessary to study other types of motivations, such as strategic and/or family ones that, based on the results obtained, could be relevant to justifying the desire to grow in FBs. On the other hand, this desire to grow can materialise in strategies other than the international one and that would also be of great interest to analyse. Gómez-Mejia et al. (2010) point out the negative impact on diversification of family control in a company – an impact that is attenuated by the increase in business risk. The study of diversification in family olive and wine companies would be of interest, given the remarkable diversification of their offers in recent years, as in the case of their opening to tourism, towards which a greater and greater number of olive oil mills and wineries are increasingly directed (De Salvo et al., 2013). Third, while the Spanish wine and olive oil production companies represent a highly relevant research setting the generalizability of these results may be limited. In Spain, we can observe a strong presence of companies in both the family and international sectors. Future research should delve into whether the relationship between family involvement and firm growth changes when considering other measures and firms from other countries and/or industrial sectors.

CONCLUSIONS

Our study tests two hypotheses based on the theoretical relationships between family involvement, business growth, economic motivations, and international strategy. The first hypothesis to test whether economic motivations mediate the relationship between family involvement and firm growth in both the wine and olive sectors arises from the literature that studies the role of economic objectives and business growth of family companies. The second hypothesis tests the role played in both sectors by the internationalisation strategy as moderating variable in the relationship between family involvement and firm growth. Therefore, it adds internationalisation as a growth strategy, testing the importance of economic motivations in the propensity towards the development of an internationalisation strategy in internationalised and non-internationalised Spanish olive oil mills and winery companies. The results of our analysis support the first hypothesis, pointing to the main role of economic motivations in the pursuit of business growth. However, these economic motivations only fully explain the business internationalization in internationalised wineries since, for non-internationalised companies in this sector and for all the companies in the olive sector (international and non-international), the economic motivations only partially justify the growth of these companies. In this way, economic interests fully mediate the relationship between family involvement and business growth in international wineries, whereas this explanation is partial in both non-international companies and olive oil mills.

Acknowledgements

We are indebted to the associate editor and the two anonymous reviewers for their insightful and developmental feedback. Authors thank the financial support of Santander Universidades through the Santander Family Business Chair of the University of Jaén (Spain). We highly appreciate also the financial support from MCIU/AEI/FEDER-UE under Grant number RTI2018-097579-B-100.

Several indicators load between 0.40 and 0.70, which indicates that they might otherwise be considered for removal based on the CR and AVE. However, because the CR and AVE exceed the threshold, we conclude that the removal of indicators from the model with loadings 0.40-0.70 is unnecessary.