1. Introduction

Firms can search for capital, goods, knowledge and technology anywhere in the world. Markets openness and better transport and communications systems accelerate economic activities, and, hence, a firm’s location could lose some of its importance (Porter, 1998). However, firms’ location remains an important issue stimulating the topical and growing research agenda in the study of clusters (e.g., Bell et al., 2009; Engelstoft et al., 2006; Hervas-Oliver et al., 2015; Roig-Tierno et al., 2019) or, more generically, the vast strand of literature assessing the impact of geographic proximity on innovation (Faria et al., 2015; Laursen et al., 2012), entrepreneurship (Barbosa & Eiriz, 2009b; Müller & Korsgaard, 2018), productivity (Henderson, 1986), learning (Tallman et al., 2004), firm’s growth (Barbosa & Eiriz, 2011), performance (Folta et al., 2006), and strategy (Eiriz, 2020).

The resurgence of location as an important driver of economic growth and performance is justified by the role attained to immobile resources – knowledge, skills and institutional and organizational structures (Breschi & Malerba, 2001). In particular, spatial clusters of firms, usually small and medium sized enterprises (SMEs) interacting with each other, lead to changes in the firms’ competitive environment. According to several authors (e.g., Porter, 1998; Roig-Tierno et al., 2019), clusters affect competitiveness by promoting cost and productivity advantages for local firms through their positive impact on firms’ innovative capacity, due to the interaction with other actors, knowledge spillovers and the transfer of tacit knowledge, and by stimulating the creation of new businesses that diffuse and strengthen the cluster itself. According to this view, firms belonging to a cluster may have a superior performance and a competitive advantage.

The entry of new firms into a cluster, and in particular the entry of multinational companies (MNCs) is likely to affect competition, and the local firms’ strategy and performance due to changes in the competitive environment. Elekes et al. (2019) has analysed the role of MNCs on structural changes in regions regarding their contribution to the diversification of economic activity at the regional level. By assessing the impact of MNCs’ entry on local firms’ strategy and performance, this study adds to the knowledge on MNCs’ impact on specific regions, by addressing the changing nature of competition and local firm’s strategic responses.

From the perspective of local SMEs, MNCs entry into a cluster can benefit them since local businesses can observe MNCs’ technologies, practices and strategies and, therefore, they may have the opportunity to incorporate this new knowledge into their own operations (Barbosa & Eiriz, 2009a, 2009b; Blomstrom & Kokko, 1998). Assuming that MNCs yield positive effects in the places where they settle, competition with local SMEs can effectively improve their performance. However, local SMEs could also face an increasing and changing nature in competition due to the MNCs’ entry. Product market competition pressure on local firms tends to lower prices, thereby forcing them to react and increase efficiency. Local firms can no longer be passive recipients of technological spillovers (Chang & Xu, 2008), as they have to compete with MNCs either on product or factor markets. In particular, in the case of asset seeking MNCs aiming to gain access to local resources and competences to improve their position in global markets, MNCs may exert relevant competitive pressure on local firms through factor (input) markets, in particular on the labour market (Barbosa & Eiriz, 2009b).

Despite the vast literature on the impact of MNCs on the host economy or region and on the formation and evolution of clusters, to our knowledge no paper has yet integrated both strands of the literature in order to examine the extent to which MNCs entry induce incumbents’ strategic responses and assesses in which way incumbents’ strategic responses affect their performance and, hence, the cluster configuration and evolution. By attempting to understand how incumbents’ strategy is driven by changes in their local competitive environment induced by an MNC’s entry, this study contributes towards the knowledge on the strategic responses of firms located in clusters and its impact on the cluster itself. Thus, it offers an original view on the impact of MNCs’ entry on the SMEs’ strategy of local firms blending together contributions from different strands of the literature on MNCs, clusters and SMEs’ strategy.

To sum up, our main research question is to analyse incumbents’ strategic responses to a MNC’s entry into a cluster. In particular, this study contributes to the existing literature on clusters, strategy and MNCs by assessing (i) how local firms, predominantly SMEs, respond to the MNC entry, (ii) which firm-specific characteristics explain their strategic response, and (iii) the impact of incumbents’ responses on their performance. Therefore, this study offers an original approach to investigating strategic responses by incumbent SMEs towards a particular type of entry into a cluster, a MNC, which possesses firm-specific advantages relating to size and economies of scale, technological know-how, marketing and managing skills, reputation, among others (Aitken & Harrison, 1999). Moreover, the chosen MNC – IKEA – is the world’s largest retailer in the furniture industry, having a global positioning. On the contrary, incumbent SMEs are part of the Portuguese furniture cluster, being focused on local markets and less connected to international value chains. Thus, important effects of IKEA’s entry, through the establishment of three factories, are expected on the strategy of local SMEs, although the nature and extent of those effects are unknown so far, reinforcing, therefore, the contribution and relevance of this study.

The rest of the paper is organized as follows. The next section presents the literature review and theoretical framework. Section 3 describes the context of the study in the largest cluster of furniture production in Portugal as well as the method adopted in this research. Section 4 presents and discusses the results. Finally, Section 5 identifies contributions, limitations and suggestions for future research.

2. Literature review and theoretical framework

2.1. Clusters and firm heterogeneity

A cluster is an agglomeration of firms in a sector and related sectors that are located in a particular place or region. Given that this concept can encompass different meanings and interpretations, for the purpose of this research, the concept of cluster adopted is the Marshalian industrial district (Markusen, 1996, p. 293), comprising fundamentally “small, innovative firms, embedded within a regional cooperative system of industrial governance which enables them to adapt and flourish”. Among the main characteristics of this type of cluster, we highlight the following: firms are predominantly SMEs but some clusters include large companies such as multinationals; they are predominantly locally owned and make their decisions (e.g., investments, production) locally; economies of scale are relatively low; there are continuous interactions between local firms both as buyers and sellers as well as by cooperating and sharing other local resources such as labour, training, knowledge and specialized services (e.g., machinery, repairs, marketing); and many firms develop collective strategies such as exports and international strategies promoted by industry associations and public entities (Eiriz, 2020).

Local firms in a cluster share a set of relatively immobile resources – knowledge, skills and institutional and organizational structures – but they largely differ in capabilities and strategies. Local firms are heterogeneous in size (ranging from micro-firms to medium-sized firms, and, in some cases, large companies), level of specialization and diversification (some of them are specialized in only a product or service while others have larger portfolios of products and services) and in their market positions (some may act locally, while others expand to other markets and countries).

Among local firms, some larger firms, including multinationals, tend to assume a leading role with a dominant position. These firms are important for the cluster as a whole because they organize production among smaller firms often by subcontracting them; they lead the process of innovation by introducing new technologies and products, thus disseminating knowledge; and they are at the forefront of market expansion and internationalization (Giuliani, 2011; Lazerson & Lorenzoni, 1999; Morrison, 2008; Parrilli, 2019).

The development of clusters has led to the emergence of entrepreneurial ecosystems involving complex networks of relationships between individuals and organizations, including different types of firms (micro, small, medium, large, national, multinational, services, manufacturers, investors, etc.) and institutions (universities, research institutions and laboratories, governments, municipalities, industry associations, etc.) that interact with each other and, in the case of local ecosystems, benefit from spatial proximity (Autio et al., 2018; Colombo et al., 2019; Eiriz, 2020; Neumeyer et al., 2019). The patterns of interaction between firms are complex, they include both collaborative and competitive relationships, and have the potential to impact on the firms’ performance.

2.2. MNCs and clusters

Overall, the entry of MNCs can benefit the local economy through job creation, training, technology transfer, contribution to the balance of payments by encouraging international trade, creating demand expectations, entrepreneurship stimulus and effects on suppliers, customers and competitors (Dunning, 1993; Enright, 2000; Hallin & Lind, 2012). Those impacts depend on the nature and shape of the firms’ assets, local resources, local firms’ absorptive capacity, and the organizational tools through which the MNC and local firms and agents interact (Enright, 2000).

Looking to MNCs into clusters, Nachum and Keeble (2003) pointed out that MNCs subsidiaries could get specific assets and resources directly from their parent firm, and, because of that, subsidiaries are more likely to be detached from the cluster and considerably differentiate themselves from local firms belonging to the cluster. Nevertheless, there are MNCs subsidiaries that interact intensively with local firms and develop local relationships similar to those established between local firms. This behaviour depends on the strategic motivations underlying the MNC’s location decision – which could be generically categorized into market seeking or asset seeking – and could engender different strategic responses by local firms. In spite of that, the relationship between a MNC and local firms may be more complex. For instance, Belussi (2018) analysed the entry modes of MNCs in relation to each of three cluster life-cycle phases (origin, development, maturity) noting that some clusters in emerging countries were founded by MNCs. When this happens, local firms emerge and act mostly as suppliers of MNCs, while in some other cases, local firms became MNCs, suggesting that they reinforce their competitive positions and explore new business opportunities.

On the other hand, MNCs pressured by stronger competition would look for “pockets of valuable resources” in peripheral areas contributing to the emergence of local clusters (Mudambi & Santangelo, 2016). When this happens, MNCs need to implement local strategic decisions that explain the emergence of local clusters in such non-traditional areas, thought some emerging clusters may fail to evolve and mature. In a context of resources seeking MNCs, the entry of MNCs that enjoy market power, either on the product market or the factor markets, imposes additional competitive pressure, affecting market prices that would force local firms to react and increase efficiency or exit the market, originating a “crowding-out effect” on local firms (Barbosa & Eiriz, 2009b; De Backer & Sleuwaegen, 2003; Spencer, 2008).

Recognizing the importance of MNCs in cluster development, Rugman and Verbeke (2003, p. 156) differentiated among the roles of MNCs depending on the way core local firms are structured as being symmetric or not, and the impact of “transborder elements”. While the role and heterogeneity of local firms was discussed in the previous section, “transborder elements” include R&D investments, access to assets, skills, routines and knowledge, or the high international visibility and credibility promoted by investments of large MNCs that may result in other foreign investments.

When a firm belongs to a cluster, it wants to access certain resources that are more easily and efficiently provided externally than internally. The access to these resources becomes more effective due to geographical proximity. As a result, the cluster is affected by factors such as MNCs connections in the local labour market; relationships with suppliers and customers; networking, collaboration and competition with other firms and other local organizations; and collective learning and creativity (Nachum & Keeble, 2003). Based on a longitudinal case study in a medical devices cluster in Ireland, Ryan et al. (2021) showed how the studied cluster evolved towards an entrepreneurial ecosystem, stressing the role of MNC subsidiaries and their partnerships with local university research centres and local firms found by ex-employees of the subsidiaries.

In spite of these contributions, the role of MNCs in clusters remains an under-researched topic (Mudambi & Swift, 2012). For instance, the literature on international business and innovation focuses on the rational and processes of innovation and interaction between MNCs and local firms but we still need to understand how that interaction and innovation influence local firms’ strategy both individually and collectively, particularly when those firms are predominantly SMEs.

Moreover, much of the literature is focused on MNC strategy but the reaction of local SMEs, which are affected by the entry of a large MNC for the first time, still needs further research. It is likely that the upgrade of strategies by local firms requires resources, specific competencies, and new and valuable knowledge possibly existing outside the cluster. Here, the MNC may play a crucial role as gatekeeper of such knowledge and, hence, fostering new competitive positions for local firms. On the other hand, downgrading strategies may become an alternative in which local firms may become suppliers of large firms and MNCs. These different patterns of evolution of local firms depend not only on their capacity and behaviour but also on the MNC strategy within the cluster, which may be more or less favourable in developing opportunities for local firms.

In particular, a MNC can adversely affect local firms, constraining their opportunities. It can gain the best suppliers and distributors of goods and services, either through the use of the suppliers’ maximum capacity or through non-competitive agreements. In this sense, local firms may be forced to switch to worse suppliers and distributors, compromising their strategic advantage and giving rise to a decreasing performance and output (Spencer, 2008). This effect occurs when MNCs affect local competition in product, labour and financial markets. The entry of MNCs can also limit the access of local businesses to scarce resources, raising the prices of essential goods, including the most basic ones such as energy and water, and, hence, reinforcing local firms’ heterogeneity.

2.3. Theoretical framework on incumbents’ strategic responses to a MNC’s entry into a cluster

By incumbents’ strategic responses to a MNC’s entry into a cluster, we mean a set of strategic decisions developed and implemented individually by local incumbent firms, predominantly SMEs, to respond to the challenges (both opportunities and threats) posed by the MNC’s entry into their local cluster.

Incumbents’ strategic responses to entrants depend on the magnitude of the competitive environment changes, which, in turn, depend on firms-specific characteristics (Bamiatzi & Kirchmaier, 2014; Bell et al., 2009). The competitive environment changes could be mainly on the product market side or on the factors (inputs) market side. In the case of a MNC’s entry, the strategic motives underlying the location decision mould its impact on the competitive environment and, therefore, on the local firms’ competitive responses. There are four strategic options for firms in a cluster confronted by the entry of a MNC (Jaffe et al., 2005): attack the MNC entering the cluster; cooperate with the MNC; defend the initial position; or exit the market. The variation in the incumbents’ response might be explained by different incentives to respond towards the entry, which depends on the incumbents’ competitive position in the cluster and on their specific characteristics underlying resources and capabilities. Therefore, the incumbents’ strategic responses can be explained either by arguments from the resource and knowledge-based views or from market-based efficiency matters.

When local firms require specific advantages and operate in highly localized industries, they should adopt a defensive strategy. Local firms have to acquire vital skills and competences to defend their positions from the MNC. The alternative to this option is to exit the market. Contrarily, when specific advantages of local firms, based on specific resources and competences, are high, a possible strategy is to attack the MNC, competing in its relevant market. In a context of strong globalization, the strategic option of attacking the MNC’s competitive position would imply entering or expanding in international markets. This strategy based on stimulating exports by seeking to increase market shares could be grounded on product differentiation or cost leadership.

In the context of strong globalization and local firms with reduced specific advantages, the best strategic option for local firms could be to cooperate with the MNC. In this case, one of the best strategies is to form alliances to access the MNCs’ resources (Jaffe et al., 2005; Poulis et al., 2012). The formation of strategic alliances provides one of the best opportunities for knowledge transfer between MNCs and local firms, contributing to improve the local firms’ resources and knowledge. This knowledge mobility based on interaction between firms provides knowledge diffusion towards local firms. That is to say, that the advantages associated with knowledge diffusion and absorption are not just for the firms participating in the alliance, but also for other firms in the cluster through their interaction with MNCs and their partners (Spencer, 2008).

The competitive strategy can therefore take offensive or defensive responses in order to achieve a certain position in the industry and to obtain a higher performance and gain a competitive advantage. In this sense, Porter (1985) identified three generic strategies: cost leadership, differentiation and focus. The three generic strategies involve different ways to achieve a competitive advantage. While cost leadership strategies and differentiation seek a competitive advantage in a wide target market, focus strategies seek advantages in costs or differentiation in a restricted target market. The specific actions needed for the implementation and the effective adoption of each strategy depend on industry-specific characteristics, local firms’ characteristics and their matching with the MNC’s characteristics and its underlying strategic motivation regrding the location decision. Porter’s classic model remains the most robust and simplest model for understanding generic strategies and responses of local firms to the entry of a MNC. The model also has the advantage of being the most popular and easily understood among owners and managers of incumbent local firms.

Together with the most up-to-date model by Jaffe et al. (2005) presented before, this study proposes a typology of strategic responses by expanding those contributions and blending them with other contributions (e.g., Poulis et al., 2012; Spencer, 2008). From the previous discussion, it is expected that incumbents faced with a MNC entry into their cluster may respond with nine strategic responses: attack the MNC; cooperate with the MNC; defend the firm’s position; acquire competences; product differentiation; cost leadership; cost focus strategy in an industry’s segment; differentiation focus strategy in an industry’s segment; and internationalization. This typology was developed in order to ask local firms how they responded to the MNC’s entry. Therefore, although theoretically, exiting the market is an option, it was not assumed because such an option represents failure, whereas strategy and strategic options aim to achieve success.

Another important topic to understand incumbents’ strategic responses to a MNC’s entry into a cluster is to evaluate the perceived effects on incumbents’ performance of each of the nine strategic responses. In other words, heterogeneous performance effects are expected (Martin & Javalgi, 2019; Pett et al., 2019) among strategic responses, meaning that probably some of the strategic responses produce better performance indicators in incumbents than others. Nonetheless, it would be difficult to predict which strategic responses are better at performance-enhancing.

3. Context and method

3.1. Empirical context

The largest cluster of furniture production in Portugal, located in Paços de Ferreira and Paredes, two municipalities in the north of the country near the second largest Portuguese city (Porto), is the context selected to research local firms’ strategic response to a MNC’s entry into a cluster. The choice of this cluster was based on its structure and characteristics and on the challenging competitive environment after the MNC entry with the establishment of three factories.

The world’s largest furniture retailer, the Swedish IKEA, has installed in the Portuguese furniture cluster, three large factories in 2007, after entering in the Portuguese retail market in 2004 and achieving a significant sales growth in the southern European markets. The essence of IKEA’s supply consists of furniture, home furnishings and home utilities based on simple design of Nordic inspiration, great functionality of products and low prices. The low prices derive from the simplicity of its products and services, and economies of scale in purchasing and production. IKEA’s decision shows the importance of the Portuguese cluster in the furniture production industry.

Two main factors can be identified as the motivators to attract IKEA to enter the Portuguese furniture cluster. One of them is the cluster’s geographical proximity to ports and airports along with the proximity to some of the largest manufacturers of wood-based panels, a crucial production input to IKEA. The distance of IKEA production factories to one of Portugal’s major seaports – the Port of Leixões – and the international Porto Airport is less than 40 kilometres, served by motorways. The other factor is the large pool of skilled employees and strong technical knowledge relating to wood available in the cluster, given its long tradition in such economic activities, offering to IKEA an easy access to relevant human and technological resources. The availability of resources leads the Portuguese IKEA subsidiary to be involved in the local chain, establishing strong relationships with local firms either inside or outside the cluster. The local firms’ absorptive capacity of IKEA’s modus operandi has been the crucial factor in shaping the relationship with local firms and the intensity of IKEA’s involvement in the local chain. Therefore, the strategic motives underlying IKEA’s location decision seems to be the access to local resources and competences to improve its position in global markets. Consequently, the IKEA’s entry is very likely to engender competition pressure, in particularly, on the factor markets, forcing local firms to react in order to survive and grow.

In order to better understand the empirical context and to reinforce the research interest in analysing the Portuguese furniture cluster, Table 1 shows some characteristics of the cluster, emphasising the period before and after IKEA’s entry.

The cluster comprises mostly local micro enterprises and SMEs, which make their strategic decisions locally, developing continuous interactions, sharing local resources (e.g., labour, training, services) and contributing towards the development of collective strategies (e.g., organization of local fairs; participation in other fairs abroad) that are explicitly promoted by industry associations with the support of public entities. Most importantly, the local firms’ average size is extremely small compared to IKEA, suggesting that the MNC’s entry could engender changes in the cluster’s structure and business environment dynamics. However, these features remain after the MNC’s entry, suggesting that no noticeable changes on the structure of the cluster have occurred. Similar findings emerge when one looks at turnover as a measure of the firm’s size, indicating that the MNC’s entry appears to not significantly foster, on average, local firms’ growth and performance.

On the contrary, from the first year, IKEA is the largest firm in the cluster, reporting a subsequent increase in turnover, market share, and its distance to the second largest firm. As IKEA’s production is exclusively to supply its stores, it is likely that the three Portuguese factories supply stores in several countries, predominantly European countries, indicating its high exporting intensity profile. Nonetheless, after the entry of the MNC, the entry rate of new firms is considerable, leading to an increase in the share of young firms and suggesting a churning process of firms at work. This process of renewal and re-allocation of resources could impact significantly on the cluster’s dynamics.

3.2. Data, population and sample

In order to understand the entry effects of a MNC into a cluster, the population of this study comprises firms belonging to the furniture cluster located in Paços Ferreira and Paredes, Portugal. As explained before, both local firms and the selected MNC – IKEA – suit particularly well for the topic under research.

Primary data collection was carried out by a questionnaire. Based on the literature reviewed in section 2, firms were inquired about changes in their performance indicators after IKEA’s entry into the cluster as well as on strategic options chosen by them to respond to IKEA’s entry. The period before and after IKEA’s entry was considered in order to assess changes that took place after IKEA’s entry into the cluster; that is, after 2007. The evolution of firms’ performance indicators was analysed over the 2005-2013 period, which allows us to evaluate long-term impacts. Apart from questions related to firm-specific characteristics (e.g., size, age, location) and questions related to respondent-specific characteristics (e.g., job), the questionnaire included nine closed questions relating to motivations for locating at the cluster, markets, strategic changes and responses after IKEA’s entry, and firm’s performance. Five of the questions are based on a 5-point Likert-type scale.

A pre-test was performed in order to assess whether there were any errors, poorly constructed questions and/or some difficulty in interpretation. The research team carried out the pre-test firstly by consulting other researchers and asking their advice on the questionnaire. Then, two firms were asked to respond to the questionnaire, which allowed for some improvements in the way questions were formulated. The revised questionnaire was applied online through the Qualtrics platform on March, 3rd, 2015. Four reminders were sent over the following weeks (March, 10th; March, 17th; March, 25th; April, 1st). Firms were always contacted by e-mail with a small message describing the aim of the research and providing a link to the questionnaire. Finally, as a measure to improve the number of responses, 50 telephone contacts were chosen at random to ask for their responses to the questionnaire.

The D&B database, a major business enterprise database in Portugal, was used to systematically explore online contacts of firms belonging to the cluster under study (firms located in Paços de Ferreira and Paredes). The population comprises 400 firms for which an e-mail address was collected. Among the 400 contacts, 50 messages were returned to sender because they had the wrong address and/or were no longer in use. From the 350 firms effectively contacted, a sample of 66 valid responses for data analysis was comprised.

Despite the careful data collection procedures, including repeated response requests and telephone contacts, the total number of 66 responses was less than desirable. Nonetheless, the response rate (18.9 per cent of the surveyed firms that have provided a valid answer to the questionnaire) was indeed higher than usual for this kind of study. As a low response rate does not necessarily undermine the sample representativeness, Table 2 compares individual and organizational characteristics that are commonly assumed to be related to response patterns, in the population and sample, in order to evaluate the sample representativeness and to analyse potential response bias.

Overall, the distribution of characteristics of the respondents fairly reflects the target population and their individual characteristics ensure knowledgeable answers. Among the 66 respondents, 56 (84.8 per cent) are firm’s managers, administrators or directors. The vast majority (64, 96.9 per cent) have been working in the sector for at least three years. Together, these two indicators suggest that respondents were experienced individuals, with knowledge and prominent positions in their firms, and have a good understanding of the cluster and its competitive environment.

On average, the sampled firms had 29.6 employees, with the largest one having 240 employees, which is notably above the average population size. This discrepancy between the sample and the population is explained by the predominance of SMEs in the sample, while the population comprises a huge share of micro firms. This overrepresentation of SMEs would not lead to a relevant potential selection bias, as micro firms are less prone to independently react to a MNC’s entry. Their production activities are usually dependent on other firms’ production and management decisions, leading to no strategic response to a MNC’s entry. Instead, the sample is comprised of a larger share of incumbent firms (age above 6 years old) than the population, suggesting that respondents’ firms have market experience and their answers are potentially more informed, which could reinforce the validity of the empirical results. In fact, the sampled firms have some seniority (average age of 23.2 years old), which provides them with enough competitive and survival experience in the sector.

Looking at international exposure and experience, 89.4 per cent of the surveyed firms have some international experience. The share of firms that operate exclusively in foreign markets is of 21.2 per cent, while 10.6 per cent of them operate exclusively in the domestic market. In turn, the number of firms operating simultaneously in both markets is of 68.2 per cent.

3.3. Empirical variables and econometric approach

The empirical variables and the econometric approach chosen are directly related to the research questions and the ability to produce reliable estimates.

Firstly, in order to analyse the local firms’ strategic responses towards MNC’s entry, firms were asked to identify their strategic responses. For this purpose, one of the survey questions identified nine strategic responses discussed in the theoretical framework: (1) attack the MNC (competing with IKEA in its market); (2) cooperate with the MNC (developing alliances); (3) defend the firm’s position; (4) acquire competences to gain advantage; (5) product differentiation; (6) cost leadership; (7) cost focus strategy (in an industry segment); (8) differentiation focus strategy (in an industry segment); and (9) internationalization, and asked respondents to answer Yes/No for each of them. Based on that, the empirical dependent variables take value 1 when a local firm answers “Yes”, reporting to have pursued a given strategic response towards IKEA’s entry, and 0 otherwise.

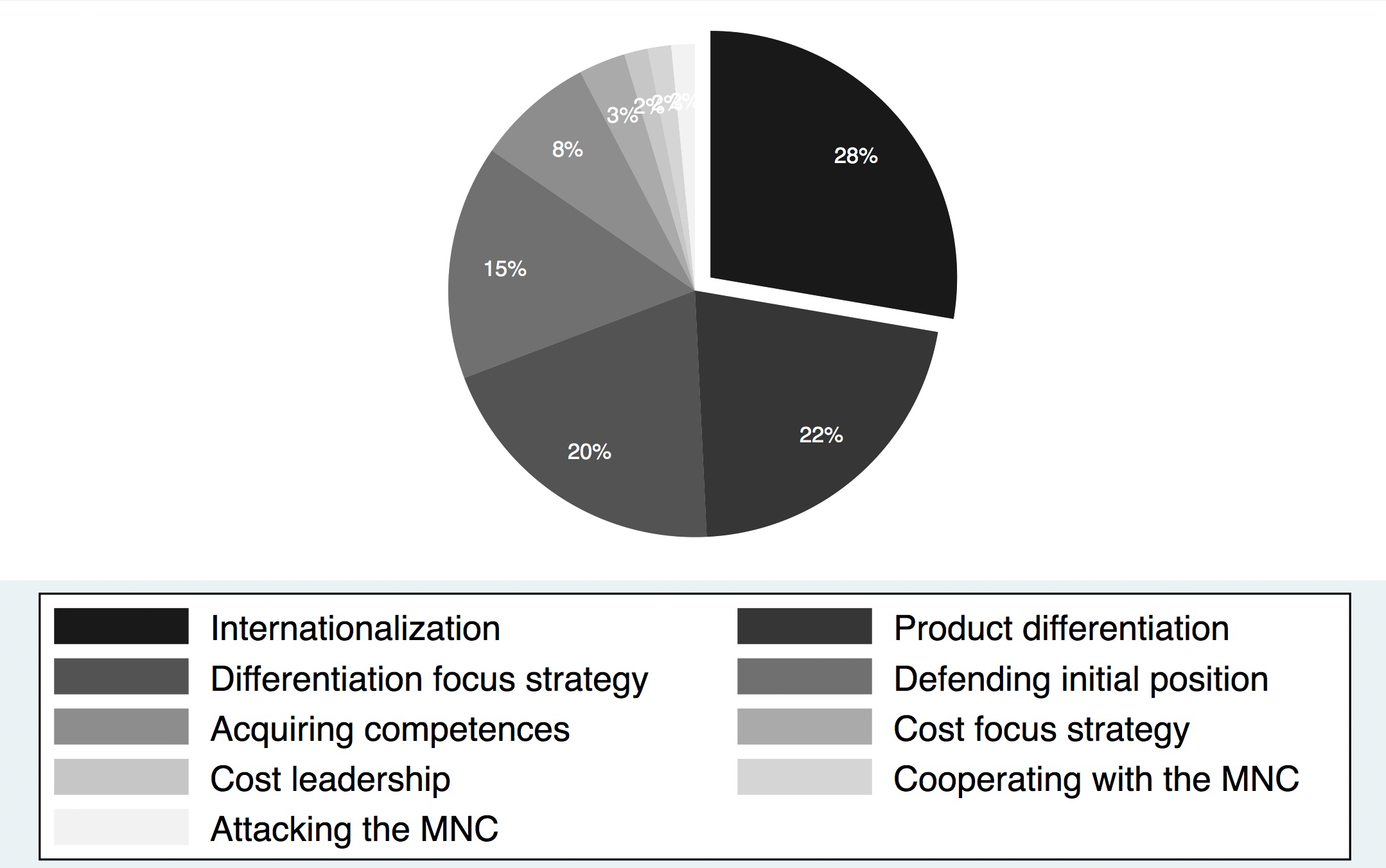

On the econometric approach side, the nature of the dependent variables - a binary answer (0/1) derived from the survey question related to the adoption of a given strategic response - suggest the use of logit regression models, in which the probability of adopting a given strategic response is modelled as a function of firm-specific characteristics that could disclose differences on resources and capabilities among firms. A different logit regression model was estimated for each of the five most frequently adopted strategic responses (i.e., internationalization; differentiation focus strategy; product differentiation; defending initial competitive position; and acquiring competences to gain advantage; see Figure 1) in order to identify which firm-specific characteristics explain strategic responses towards MNC’s entry.

Therefore, here, the explanatory variables intended for measuring firm specific characteristics are age, size, market and a locational factor. The locational factor aims to ascertain the main motivations for a firm to be located in the cluster, which was one of the questions in the questionnaire. It takes value 1 if a firm identifies the availability of skilled employees in the cluster or if that firm identifies the geographical proximity of firms operating in related sectors as the main motivation underlying the location decision, and 0 otherwise. The size variable is computed as the logarithm of the total number of employees, while the SME variable is a binary variable that takes value 1 if the number of employees is higher than 10 and lower than 50 employees and 0 otherwise. The market variable is also a binary variable that takes value 1 if the firm operates in the domestic and international market and 0 otherwise. The age variable is the number of years from a firm’s creation until 2015.

Secondly, the assessment of a firm’s strategic response effects on performance was based on dependent variables related to performance indicators derived from a multiple item-question measured by a 5-points Likert scale. For each performance indicator defined according the existing literature (e.g., Chakravarthy, 1986; Murphy et al., 1996), each possible value of the Likert scale represents an order on the respondents’ perception on firm’s performance evolution before and after IKEA’s entry. For that, respondents were asked about the evolution of some performance indicators between 2005 and 2013. As a result, it requires the estimation of ordered logit models, a different econometric approach, in which the five strategic responses adopted by the firms (see Table 5) are the variables of interest, that is, the variables that directly test the statistical association between strategic response and performance. In order to account for differences on firm’s resources and capabilities that would additionally affect performance, the control variables size and locational factor were also included on the empirical model. This econometric approach allows us to evaluate the perceived effects of each strategic response on a vast array of performance indicators and, therefore, to disclose whether there are heterogeneous performance effects among strategic responses.

4. Empirical results and discussion

To begin the empirical analysis and discussion, we have performed a diagnostic evaluation in order to assess the statistical validity and reliability of the estimates and the empirical findings. Then, the empirical results were presented and discussed.

4.1. Diagnostic on statistical validity and reliability

First of all, the issue of the small sample size deserves further attention that goes beyond its representativeness discussed in section 3.2. The main consequences of a small N are larger standard errors, which lead to lower t-statistics and a failure to reject the null hypothesis when false, and the high sensitivity of the estimates to small changes in the sample composition. By carrying out the condition index test (Belsley, 1991), which indicates severe linear dependence between variables when the index exceeds 30 and a moderate to severe sample problem for index values between 10 and 30, the sensitivity of estimates to sample composition changes is assessed. The condition indexes are 5.79 and 6.11, for models in Table 4 and Table 5, respectively, values below the suggested bounds and indicating that the small sample size would not have a significant impact on the reliability of our results. On the other hand, the potential problem related to statistical power does not seem to be of concern, since several independent variables’ coefficients are statistically significant.

Nonetheless, the estimates of interest should be read with caution (see Table 4 and Table 5). The cross-section nature of the survey data prevents us from carrying out a proper analysis of causality given that it is tricky to deal with potential econometric endogeneity. The estimates should not be interpreted as measuring a causal effect but rather as capturing a correlation of which the causal effect has but one possible interpretation. Moreover, the variables of interest – those related to strategic responses – are reported to a period near IKEA’s entry (that is, 2007), while performance indicators were assessed several years later. This gives to the variables of interest a lagged and predetermined nature that helps to mitigate a potential econometric endogeneity problem.

On the other hand, several preventive steps to minimize the potential for common method bias, which ultimately could result in an endogeneity problem, were taken. Following Chang et al. (2010) and Podsakoff et al.'s (2012) recommendations, at the survey design stage the questions in the survey followed a random order and different scale types were used in order to avoid a biased pattern of responses from individual raters. Moreover, respondents were assured of the anonymity and confidentiality of the study, which should induce answers as trustworthy as possible. On the statistical analysis stage, the econometric approach, based on non-linear models, adds complexity to the relationship between the dependent and independent variables that prevents a potential common method bias, as respondents are unlikely to visualize and anticipate the non-linear effects under scrutiny. Therefore, these ex-ante and ex post procedures have the potential to assuage possible concerns related to common method bias.

4.2. The cluster and the entry of IKEA

Being located in a cluster has a long-lasting effect on a firm’s competitive strategy and performance. In order to demonstrate the relevance of that long-standing choice, firms were asked to rank the relevance of some location factors. All firms indicated that they had always been located in the cluster, suggesting that the location in the cluster was a first and long-standing choice. On the other hand, the relevance of some location factors seems to vary significantly among local firms.

The main advantages identified relate to accessing resources and specialized technologies and to improving productivity, suggesting that localized spillovers could be at work. Nonetheless, some locational factors seem to divide respondents in terms of their relevance. For instance, the creation of new business opportunities appears not be greatly recognised as a relevant locational factor, casting doubts on the role of a cluster in fostering entrepreneurship.

Looking at internationalization, belonging to the cluster appears to be a factor that is perceived as facilitating the internationalization process. More importantly, IKEA’s entry seems to have boosted the local firms’ exporting intensity. In the 2008-2013 period, respondents report, on average, a 14.9 per cent points increase in the share of exports, suggesting that the IKEA’s entry in 2007 might have had a positive effect on the firms’ exporting performance. Nonetheless, there are other explanatory factors, namely some shrinkage in the domestic market during 2008-2013, making it difficult to establish a cause-effect relationship between IKEA’s entry and the degree of internationalization of local firms. In any case, it is very likely that IKEA’s investments in the cluster brought greater visibility to local firms, which may have favoured their international performance.

In order to understand the firms’ performance before and after IKEA’s entry, Table 3 reports respondents’ perceptions on the evolution of those indicators.

Overall, the results show that firms in the cluster, when faced with IKEA’s entry, reported slight changes in their performance, probably encouraged by the MNC’s challenge. Incumbents’ response usually relates to the use of imitation and skills development (Hallin & Lind, 2012), yielding changes on performance indicators mainly related to improvements on the firms’ competences. Nonetheless, changes in the local firms’ performance seem to be spread out over all the indicators, making it difficult to identify a well-defined path of performance gains.

Moreover, an interesting finding is that, during the 2005-2013 period, IKEA’s does not seem to have caused an upward effect on wages, even though firms’ competences have, on average, significantly evolved. IKEA’s strategy could provide important clues towards an explanation. In fact, IKEA bases its strategy on low costs and, as a result, it is not expected to cause an upward effect on the local labour market. Local wages – low wages comparatively to many European countries –, coupled with skilled employees, has been one of IKEA’s location factors in the cluster.

4.3. Effects of IKEA’s entry on local firms’ strategy

The entry of IKEA on the Portuguese furniture production cluster prompted incumbents to adjust their strategies. In order to assess local firms’ strategic responses following IKEA’s entry, incumbents in the cluster were asked to specify their strategic responses towards the entry of IKEA. Figure 1 shows the distribution of the nine strategic responses, derived from the literature and listed on the survey, adopted by local firms. The possibility of some of those strategies occurring in the absence of IKEA’s entry is very unlikely. To prevent that possibility, an open question in the survey allowed, if applied, to ask firms to explicitly report that the IKEA’s entry had a different (or, even, no) effect on their strategies. Here, only strategies reported as direct responses to IKEA’s entry were considered.

Overall, local firms revealed the adoption of a large diversity of strategic responses towards IKEA’s entry. The largest share of firms internationalized their business as a strategic response, while the less adopted strategic responses were attacking the new entrant and competing with it in its market, cooperating with the new firm through the establishment of alliances and cost leadership. The other two most frequently adopted strategic responses were product differentiation, and differentiation focus strategy. This suggests that local firms, which are heterogeneous, reacted diversely to IKEA’s entry and intend to move away from IKEA’s competitive positioning in order to generate performance gains.

In order to understand whether firm-specific characteristics explain the probability of adopting a strategic response, several logit models were estimated. For each of the five most frequently adopted strategic responses, Table 4 shows the estimated marginal effects, along with standard errors, of firm-specific characteristics on the probability of adoption.

Overall, locational factors appear to be significant in explaining firms’ strategic responses. Firms that identify the availability of skilled employees in the cluster or the proximity of other firms in related sectors to the furniture industry as important are more prone to react through a differentiation focus strategy or by defending its initial competitive position than other local firms. This suggests that those local firms value local resources and agglomeration economies, viewing them as crucial to their competitive advantage and perceive IKEA’s entry as a dispute for those resources. On the other hand, those local firms are less prone to react to IKEA’s entry through internationalization, comparatively to local firms that value other locational factors. Together, these empirical findings appear to indicate that local firms that mainly support their competitive advantage on local resources, knowledge and relationships with other local firms tend to react more locally by defending the initial competitive position or by implementing a differentiation focus strategy.

As local firms grow, and holding everything else constant, it seems less likely for them to react to IKEA’s entry by defending the initial competitive position. Instead, as local firms grow, the pressure for globalization, together with the entry of a global supplier of furniture into the cluster, appears to favour internationalization or a differentiation focus strategy, as suggested by Jaffe et al. (2005), Porter (1985) and Poulis et al. (2012), in spite of the statistical fragility of those findings. A possible explanation is that local firms are mostly SMEs with fewer capabilities than IKEA to explore economies of scale. As a result, local firms have a lower ability to respond by focusing on low costs, in order to replicate IKEA’s low prices (although complemented by factors such as design, service and complementary offers especially in terms of decoration and home accessories). Their strategic response seems to be a differentiation focus strategy that uses high quality raw materials and custom-made furniture (complemented with a personalized delivery and assembly), a type of offer that is not feasible for IKEA’s business model based on cost leadership.

The choice of a differentiation focus strategy allows local producers to practice higher prices and position themselves in specific market segments, not only domestically but also internationally. In other words, this strategy based on distinctive offers (products and services) could be a profitable option for local firms to respond and to differentiate themselves from IKEA. Local firms operating in the national and international markets are more likely to adopt this strategic response than firms operating only in the national or in the international markets. By adopting this strategy, local firms avoid direct confrontation with IKEA and seek to defend positions in market segments, where IKEA is itself less capable.

Another interesting finding is related to firm age. Holding everything else constant, young firms seem to be more likely to cooperate with IKEA in order to acquire competences and gain advantage than other firms. The opportunities for knowledge diffusion based on relationships between local firms and IKEA appear to be better explored as a strategic response by young firms. As local firms become older, the relevance of acquiring competences to gain advantage as a strategic response to IKEA’s entry seems to decrease, suggesting that market experience allows firms to respond in diverse ways to a challenging entry.

4.4. Effects of strategic response on firms’ performance

Another important issue is to assess the perceived impact of IKEA’s entry on local firms’ performance. A noteworthy proportion of local firms (45.6 per cent) reported that IKEA’s entry in the cluster had no impact on their performance, whereas 23.9 per cent of firms have reported a small impact. On the other hand, only a small proportion of local firms (4.3 per cent) have remarked that IKEA’s entry has significantly and negatively affected their performance. A possible explanation for these results could be found on the different sizes and market positions between IKEA and the local firms. Local firms appear to perceive IKEA’s position as very distinct and, hence, as not affecting them. Moreover, huge size differences may lead local firms to not signal IKEA as a direct competitor in the product market, avoiding a direct confrontation and, hence, showing a certain competitive complacency and/or unawareness. This competitive complacency and/or unawareness tends to occur when local firms’ performance assessment is mainly focused on product market competition (where, in fact, the position of IKEA and local firms is very different) and when the increased competition that IKEA could bring to factor (input) markets, such as the labour market, is overlooked.

Nonetheless, when asked about specific performance indicators (see Table 3), which aim at measuring the impact of IKEA’s entry in several performance dimensions, local firms report significant diversity and impact on their performance assessment. As there is not a universal best performance indicator (Delmar et al., 2003) and firms could value performance dimensions differently, perceived firm’s performance seems to be more accurately assessed by looking at separate performance indicators.

Therefore, in order to better understand the effects of IKEA’s entry on local firms’ performance, some performance indicators (see Table 3) were related to the firms’ chosen strategic responses and some explanatory (control) variables that sought to measure firm-specific characteristics. Table 5 presents the ordered logit estimates on the perceptions of the firms’ performance evolution after IKEA’s entry, using several performance indicators. Following the vast literature on performance dimensions (see, e.g., Chakravarthy, 1986, and Murphy et al., 1996), those indicators were clustered into four performance dimensions in order to assess the impact on the quality of firms’ transformations in terms of efficiency, size, resources and competences, and growth. This clustering allows for a better discussion and understanding of how the various strategic responses can influence SMEs’ performance.

Overall, only two strategic responses – differentiation focus strategy (R1) and defending initial competitive position (R4) – have been perceived as having a positive and statistically significant effect on local firms’ performance, using a diversity of performance indicators. Local firms that have adopted a strategic response based on internationalization (R2) or the acquisition of competences to gain advantage (R5) appear to link their performance after IKEA’s entry to other factors rather than their strategic response. An alternative interpretation could be that those firms were committed to adopting those strategies that would improve their performance, regardless of IKEA’s entry.

Local firms adopting a differentiation focus strategy are more likely to perceive a performance improvement after IKEA’s entry assessed in terms of employment, sales (both in volume and growth rate), innovation, product quality and competences. By adopting this strategy, local firms seem to avoid direct competition with IKEA by defining a distinct offer (products and services) and by operating in specific market segments, which appear to render performance gains. In line with Martin and Javalgi (2019), these results suggest that local firms develop resources to perform efficiently and to adapt to the new competitive environment.

Similarly, while holding everything else constant, local firms that choose to defend the initial competitive position (R4) are more likely to perceive performance gains in size (employment, sales and market share), and resources and competences (in particular, the upgrading of competences). Distinctively, those firms seem to link the adopted strategic response to efficiency gains, suggesting that IKEA’s entry led firms to search for more productive and competent ways to serve their markets. Thus, it could be said that productivity gains are a way to defend a competitive position.

On the other hand, local firms adopting a strategic response based on product differentiation (R3) appear to find it hard to obtain performance gains measured by profitability. Instead, those firms are more likely to perceive a decrease or great decrease (more than 20 per cent) in profits after IKEA’s entry, suggesting that a product differentiation strategy may require strong investments and may take time to have a positive and significantly strong impact on revenues. This finding is compatible with the difficulty of those local firms to link the selected strategic response to profit-enhancing performance indicators, such as sales, product quality, exports or market share.

Looking at specific performance dimensions, it is worth noting that local firms have difficulties in relating their strategic response to exports, employees’ motivation, wages and customers’ satisfaction evolution after IKEA’s entry. This would suggest that these performance dimensions could be driven by other factors than a specific strategic response. In fact, firm size positively affects almost all performance dimensions, indicating that large firms are more likely to perceive performance gains after IKEA’s entry, regardless of their strategic response. Moreover, and similarly to Pett et al. (2019), the relationship between strategic response and performance indicators corroborates the idea that firms have a variety of ways to grow and to perform, even in the event of such a challenging competitive entry.

5. Conclusion

Even in a global economy, location still plays a key role in firms’ strategies and performance due to interactions with other local firms and supporting organizations, agglomerations economies and knowledge spillovers. When entering a cluster, a MNC is very likely to affect the cluster business environment, in particular the context of local firms’ strategy and rivalry. In this study, the effects of IKEA’s entry into the main cluster of furniture production in Portugal were examined in terms of the incumbents’ strategic responses and changes in their performance.

5.1. Main findings and implications

On the basis of our empirical results, key findings emerge. First of all, local firms – small producers offering customized products with more added value, using different raw materials and providing delivery and assembly services – recognise that some strategic changes had been implemented in response to IKEA’s entry. Local firms’ strategies were mainly based on the search for a distinct positioning from the MNC, implementing a differentiation focus strategy whereby specializing in distinct products, value added services and positioning themselves in more restricted markets. This strategic response aims to avoid a direct confrontation with IKEA, whose strategy is based on scale economies, simple design, and low-cost materials. Therefore, in line with Javornick et al. (2018), the IKEA’s entry seems to stimulate upgrading capabilities and boost the sophistication of local firms’ production, moving them into more complex products.

Secondly, the diversity of strategic responses is explained by the main motivations to be located in the cluster and other firm-specific characteristics such as size and the presence in the domestic and international markets, which are common proxies for firm’s resources and access (and absorptive capacity) to valuable and new knowledge.

Thirdly, and more importantly, the empirical findings suggest that different strategic responses affect distinctively local firms’ perceptions of performance evolution after IKEA’s entry. A differentiation focus strategy seems to positively affect a variety of performance dimensions, either in terms of size or resources and competences, suggesting that this strategy will reinforce competitive positions and open new business opportunities. Whereas, a strategic response based on defending an initial competitive position seems to lead to performance gains mainly related to the size dimension.

Fourthly, these findings suggest that firms facing an important environmental change – the entry of a MNC into their cluster – respond in diverse ways and find alternative pathways to obtain performance gains, engendering, to some extent, structural changes into the cluster. An important theoretical contribution of this research was to test the applicability of the typology of nine strategic responses proposed in our original theoretical framework based on previous contributions to the literature (Jaffe et al., 2005; Porter, 1985; Poulis et al., 2012; and Spencer, 2008).

An important managerial implication is that firms do not have static positions. These positions evolve over time due to multiple environmental and organizational factors. These positions should be carefully managed. The entry of a MNC into the cluster is an important environmental change that can have an impact on incumbents even when they have very different market positions and strategies from the MNC. With the entry of a MNC, local firms have to deal with all sorts of effects in competition for resources and capabilities, and not only with the most evident or obvious effects. Managers should also understand and anticipate impacts on their firms’ performance, activities and strategies. In the studied cluster, a rational choice for some local firms seems to be the development of a differentiation focus strategy. However, depending on the characteristics of the incumbent, the cluster and the strategy of the incoming MNC, other strategies may be optimal.

This paper takes a relevant step towards understanding the extent to which a MNC induce strategic changes in local firms and, therefore, in the host cluster and region. As MNCs tend to be more connected to international value chains, the entry into a cluster opens the scope to local firms to upgrade competences, to be innovative and engender long-lasting changes in the cluster and region (Elekes et al., 2019; Neffke et al., 2017).

5.2. Limitations and future research

This study has some limitations that should be taken into account in future research. The main limitation is that it is based on a single cluster and a single MNC entering into that cluster. Therefore, a possible and fruitful avenue for future research would be to study multiple clusters and MNCs with different characteristics and competitive dynamics. Moreover, in order to expand our knowledge about competitive interaction between incumbents and entrants, another rewarding topic would be to analyse the impact on MNCs entering the clusters, as well as on other types of entrants.

On the other hand, the cross-sectional nature of the empirical study prevents us from analysing a dynamic evolutionary aspect in evidence. The diversity of strategic responses of local firms and their relationship with firm-specific characteristics suggests that there is an evolutionary process over the ability of firms to react and adapt to the changing environment in order to create a competitive advantage. Therefore, the detailed evaluation of heterogeneous evolutionary strategic responses of selected firms from each strategic response category would be a rewarding avenue for future research. Therefore, further theoretical and empirical studies have the ability to enrich and validate the proposed typology of strategic responses and to further our understanding of the relationships between strategic responses and firms’ performance. For instance, the proposed typology did not include exiting the market as a strategic response because such a strategic option represents failure, while, it could be argued, that the aim of strategy is success. Moreover, the empirical study of exiting is very problematic when the research focus is on incumbents, making it impossible to ask incumbents if they exited the market because, in fact, since they are part of the population of study, they have remained in the market.

The study of the impacts on strategy could also benefit from the analysis of more specific elements of a firms’ strategy. In fact, another interesting topic would be to assess which specific characteristics of the incumbents’ business models are more affected by the entry of a MNC. For instance, what are the impacts on variables such as technologies, product features, services, market segments, sources of revenue, procurement, distribution channels, cost structures, prices, branding or promotion?

In addition, while this study focused on the impacts of a MNC’s entry on the strategy and performance of local firms, it would be interesting to conduct a longitudinal research on the different effects on the host region, such as the degree of specialization/diversification of the region (Elekes et al., 2019), the patterns of the region’s evolution (Birkinshaw, 2000) as a consequence of a MNC’s entry, and the structural changes and long-lasting effects in the cluster and region (Neffke et al., 2017). These would be other fruitful avenues for future research.

Acknowledgements

The authors wish to thank the relevant contributions of the Editors and the anonymous Reviewers to a previous version of this paper. We also tank the contribution of Diana Carvalho in data collection. This paper is financed by National Funds of the FCT – Portuguese Foundation for Science and Technology within the project UIDB/03182/2020.

About the Authors

Vasco Eiriz is an associate professor of management (with Habilitation) at the University of Minho (Portugal). He holds a PhD in Management from the University of Manchester Institute of Science and Technology (United Kingdom), a Master in Business Administration from the University of Minho (Portugal); and a first degree in Management from the Instituto Superior de Gestão (Portugal). His research interests lie in the interception of strategy, entrepreneurship, innovation and business marketing. He has published in journals such as Journal of Small Business Management, International Business Review, Industrial and Corporate Change, Growth and Change, International Entrepreneurship and Management Journal, Management Decision and, among others, Service Industries Journal. Vasco Eiriz is the corresponding author.

Natália Barbosa is an associate professor of economics (with Habilitation) at the University of Minho (Portugal). She holds a PhD in Economics from the University of Manchester (United Kingdom), a Master in International Trade from the University of Minho (Portugal), and a first degree in Economics from the University of Porto (Portugal). Her research interests are in the fields of business dynamics, innovation, and foreign direct investment. She has published in journals such as Research Policy, International Journal of Industrial Organization, Journal of Small Business Management, International Business Review, Industrial and Corporate Change, Review of Industrial Organization, Growth and Change, and, among others, Economic Letters.