INTRODUCTION

The success of a nascent venture is contingent on the entrepreneur continuing to invest time in that venture. This is due, in part, to the recognition that entrepreneurship is a process that requires tending (Davidsson & Gruenhagen, 2022; Mcmullen & Dimov, 2013). Distractions pulling an entrepreneur away from their venture can take many forms, including time constraints shifting the entrepreneur’s focus (Levine & Norenzayan, 1999) and entrepreneurs simply losing interest (Shane et al., 2003). Findings of prior studies on choosing to invest time in a venture suggest that a number of important antecedents in this regard include family and business interconnectivity (Hsu et al., 2016), personal characteristics and feedback from the environment (Holland & Shepherd, 2013), escalation of commitment, how an entrepreneur frames challenges and opportunities (Miller & Sardais, 2015), and entrepreneurial passion (Cardon & Kirk, 2015). Researchers have also indicated that expectations related to outcomes might influence the decision to continue investing time in a project. Evidence to this effect has been illustrated in cases related to corporate and social projects (Mahlendorf & Wallenburg, 2013; Onifade et al., 1997), as well as in the decision-making context (Lee et al., 2015).

Although several studies have explored potential antecedents to further investment of time and resources in a project, scholars have paid limited attention to prior time invested, even though organizational behavior theory would indicate a strong relationship between activity in the two different time periods (Staw & Ross, 1987). Moreover, the literature on escalation of commitment suggests that as past time invested in a project increases, future time invested will also increase, regardless of whether the actor anticipates positive or negative outcomes (Kier et al., 2014; McCarthy et al., 1993; Staw & Ross, 1987). This is in contradition to a meta-analysis which indicated a lack of a statistically significant relationship between past and future time invested (Sleesman et al., 2012). These inconsistencies may indicate a need to re-consider the relationship between past and future time invested in the presence of, and in conjunction with, other predictors to arrive at a more comprehensive theoretical framework.

Other variables, such as opportunity confidence and business plan usage likely play a role in the amount of time an entrepreneur chooses to invest in their venture. Opportunity confidence, or a belief that the venture will be successful (Payne et al., 2009) could spur the entrepreneur on. On the other hand, a fear of loss might feel more salient, driving the entrepreneur to invest more time in the hopes of avoiding loss. Business plan usage has been shown to be associated with longevity of a venture as well as financial success (Becherer & Helms, 2009). Might it be possible that the use of a business plan would affect the level of confidence the entrepreneur has in the success of the venture? And how might that interact with preexisting beliefs related to the probability of success of the venture? The exact mechanisms for these relationships are unknown, warranting in-depth study of the literature and appropriate theorizing.

The primary research question sought to be answered in this study is: How does past time invested in a venture affect future time investment? Finding an answer to this question helps to clarify discrepancies regarding the effect prior time invested in a venture (which is deemed an important antecedent) might have on continued engagement with the business. Our research question is further motivated by findings of past research showing that the duration of time invested in a nascent venture (Davidsson & Gruenhagen, 2022) and the consistency of the efforts put forth by an entrepreneur (Timmons et al., 2004) positively relate to new venture success. Moreover, we find it more rewarding to investigate this relationship alongside exploring the roles that opportunity confidence and business planning might play as two important moderators. In this regard, we develop a theoretical model that encapsulates the proposed relationships and empirically test it using a panel data. After that, we report our results and discuss their implications.

Contributions. There are several contributions that come out of our work. First, our study addresses the discrepancy regarding the relation between past time and future time invested in a new venture by revealing a significant relationship between the two time periods. Moreover, our study sheds further light on this relationship by studying venture confidence and business planning as two important moderators. In this regard, our work finds business planning to have a pivotal role in an entrepreneur’s commitment and consistent effort put forth toward their new venture. In the same vein, this study has a practical implication regarding how to develop a business plan that can effectively address a venture’s existing, as well as anticipated, shortcomings or failures. Our study also contributes to the emerging literature on entrepreneurship as a temporal process (Davidsson & Gruenhagen, 2022) by showing how successful new venture creation attempts follow a temporal process wherein time investments in one stage encourage future time investments in a later stage. In addition, we believe the contributions of our study help enrich an emerging literature on ‘everyday entrepreneurship’ as the insights provided are consistent with experiences of average ventures, versus those with large growth potential (Welter et al., 2017).

THEORY DEVELOPMENT AND HYPOTHESES

In this section, we develop a theoretical model that seeks to provide a partial explanation of why entrepreneurs choose to invest time in a venture. For many entrepreneurs, this is likely not as much a conscious decision as an unconscious one. The escalation of commitment literature provides a basis for this research in that past effort will, most often, be a strong predictor of future effort. We also suggest that considering opportunity confidence and business planning might further help to explain this relationship. Having confidence in the venture may lead to a higher level of time invested in the venture. Additionally, higher levels of planning may also increase the amount of time that nascent entrepreneurs may invest in developing their venture.

The Importance of Time in Entrepreneurship

Although recent literature has begun to explore the impact that time investment has on new venture development, the attention it has received has been minimal (Lévesque & Stephan, 2020). The topics that have been covered range from persistence to time constraints, and the process of entrepreneurship, to name a few.

First, continued time investment is essential to the success of the venture. Nascent ventures tend to fail at a significantly high rate. Some may run out of money or have other constraints that require the entrepreneur to seek work outside their venture, but other entrepreneurs simply drift away from their venture, slowly reducing their time investment on it and finding other interests on which to invest their time (Shane et al., 2003). The chance of success increases as the entrepreneur continues to pursue their goal (Timmons et al., 2004), therefore, continued time needs to be invested in the venture. Second, entrepreneurship is a process (Mcmullen & Dimov, 2013), and processes take time. Although there does not seem to be a specific series of steps that entrepreneurs must take to succeed, there is enough evidence to conclude that they must continue to spend time developing their venture. Recent research has found that temporal aspects of entrepreneurship such as time, timing, and duration of time investment have been associated with increased success of nascent ventures (Davidsson & Gruenhagen, 2022). Next, personal time investment is a possible signal to potential partners, investors, and customers as to how seriously the entrepreneur is about building their business. For instance, a study on venture capital investments found that the venture capitalists assessed the commitment of the entrepreneur prior to choosing where to invest (Busenitz et al., 2005). Finally, entrepreneurship is a combination of skill and luck (Morgan et al., 2016; Soto‐Simeone et al., 2021). If the entrepreneur steps back too early, they might miss the luck part because they stopped too soon.

With that said, there are instances where it is not prudent to continue investing time in a venture. For instance, as the probability of success decreases, in a utilitarian world we would expect the entrepreneur to begin to look for other opportunities. But this is not always the case. Research into escalation of commitment finds that, at times, entrepreneurs will continue to persist in activities beyond the point a utility perspective predicts.

Time Investments and Escalation of Commitment

Escalation of commitment suggests that as past time invested increases, future time invested will also increase, regardless of whether the actor anticipates positive or negative outcomes. Escalation of commitment takes into consideration four primary determinants of escalation behavior (Staw & Ross, 1987). These include project, psychological, social, and organizational determinants. First, the project determinants center around the expected utility of the outcome and strongly relate to the rational aspects of a decision to pursue a given project. Second, psychological determinants related to cognitive and affective components of decision making might cause an actor to work harder to achieve a given outcome as the possibility of achieving it appears more distant. Next, social determinants include the impact opinions of others might have on decision making. Not wanting to ‘lose face,’ actors might continue a given activity beyond what might seem prudent, given the knowledge at hand. Finally, the authors included organizational determinants, such as the institutionalization of a program that may predispose the organization to continue on its current path.

Researchers have found escalation of commitment to be particularly salient among entrepreneurs (Kier et al., 2014; McCarthy et al., 1993). The following paragraphs provide supporting evidence for each of the four determinants of escalation that include: project, psychological, social and organizational determinants.

Project determinants. Entrepreneurs would not pursue a venture unless they believed, at some level, that their investment of resources had a high probability of paying off. Escalation of commitment proposes that projects with a long-term horizon for profits may have a more difficult time determining when a project is off-track (Staw & Ross, 1987). For instance, Staw and Ross highlight the story of the World’s Fair Expo '86, wherein the planners realized that, while it would be expensive to continue development, it would be more expensive to stop. While some nascent ventures may have short-term profit capability, the majority take longer to reach a profit. Additionally, some researchers have hypothesized that efficiency requirements for human capital can’t be known until an entrepreneur starts and operates a venture (Jovanovic, 1982), indicating a longer time horizon before a venture might reach profitability.

Psychological determinants. The primary psychological determinant covered in the escalation of commitment literature is that of sunk costs. The concept of sunk costs was first introduced in the economics literature, related to investments in infrastructure (Gordon, 1956), and later picked up in the psychology literature (Arkes & Blumer, 1985). The sunk cost fallacy suggests that once an actor makes investments in resources (time, money, effort, etc.), human nature compels us to continue the current course of action to avoid ‘wasting’ the resources we have invested to-date (Kier et al., 2014; Rosenbaum & Lamort, 1992). This fallacy makes it likely that an entrepreneur might continue a course of action even though immediate results do not appear financially favorable (Arkes & Ayton, 1999).

Social determinants. Entrepreneurs are cautious about not wanting to appear to waste resources (Arkes & Blumer, 1985). It can be quite difficult to admit that resources that have been expended to be a waste (Sleesman et al., 2012). In the case of entrepreneurs, their credibility and reputation are synonymous with that of the firm. If the firm fails, they may also perceive themselves as a failure (DeTienne et al., 2008). This extra pressure will also encourage entrepreneurs to escalate their commitment to the venture.

Organizational determinants. Within the context of nascent ventures, organizational determinants play less of a role. A major mechanism within an escalation of commitment is self-justification, in that decision-makers tend to seek out evidence that supports their initial decision to pursue a given route (Staw, 1981). This theory has found support within the entrepreneurship literature(DeTienne et al., 2008).

Based on these arguments, mainly that entrepreneurship contains relevant aspects of project, psychological, social, and organizational determinants, we suggest that escalation of commitment is relevant to the entrepreneurship setting. Overall, the prevalence of escalation behaviors among entrepreneurs makes them more likely to invest time and effort in their nascent ventures in proportion with the time and effort initially expended. Therefore, we state the first hypothesis of this study as follows:

Hypothesis 1: As past hours invested in a nascent venture increase, future hours invested will also increase.

Opportunity Confidence and Time Investment

Opportunity confidence is associated with a belief in the ability of the firm to succeed (Payne et al., 2009), specifically as it relates to subjectively evaluating the opportunity being filled by the venture (Davidsson, 2015). As belief in the venture increases, it would seem likely that time committed to the venture would also increase. On one hand, a higher level of belief provides an incentive that the efforts of the entrepreneur will pay off. On the other hand, the belief that the chance of failure is high might spur on the entrepreneur to work harder.

If the entrepreneur has a high level of confidence in the venture, that opportunity confidence might serve as a motivator, enticing the entrepreneur to spend more time to develop their venture, as there is a strong belief that the behavior will have a strong payoff for the entrepreneur. The overconfident nature of entrepreneurs (Hmieleski & Baron, 2009; Simon & Shrader, 2012; Stone, 1994) may lead to varying effects of venture belief on time invested in the venture, providing better clarity of escalation of commitment within the entrepreneurship context. An experiment with undergraduate students found that overconfidence did not lead to increased effort or performance (Stone, 1994). Instead, effort increased only after inducing negative expectations among the students. In this case, it appears that the lower levels of expectations might provide a greater incentive to work harder. This idea is reinforced in the entrepreneurship context by research which found that, when things appear to be going poorly, an entrepreneur is more likely to increase their time investment in order to save the venture (Davidsson & Gordon, 2016).

Overall, it appears that both low and high levels of opportunity confidence can result in an increased effort put forth by an entrepreneur to expand his/her nascent venture, with lower levels of venture confidence demanding even more effort from an entrepreneur to help the new venture survive amid the anticipated fear of business failure. Based on the above arguments, we propose the following hypothesis:

Hypothesis 2: Venture confidence positively impacts the relationship between past and future time invested by the founder, and this impact is stronger when venture confidence is low rather than high.

Business Plan Usage and Opportunity Confidence

As outlined earlier, researchers commonly assume that past behavior (such as time investment in a past period), is the best predictor of future behavior (such as time investment in a future period). As quantitative research has provided inconsistent support for this relationship, and as business planning and opportunity confidence are each strong influencers of continued involvement with a new venture, perhaps considering the interactions of these effects will provide a clearer picture of the relationships.

Referencing and using a business plan would likely increase the entrepreneur’s feelings of control, as it indicates familiarity with the topic and increased confidence in decision making. Tests of whether business planning, in and of itself, might help predict better outcomes for ventures have been inconclusive. Use of a business plan will likely help build credibility and legitimacy with external stakeholders (Honig & Karlsson, 2004) and can certainly help guide activities during the development stage (Delmar & Shane, 2003). Simply creating a business plan prior to engaging in business activities decreases the likelihood of an entrepreneur terminating their venture (Shane & Delmar, 2004). Additionally, engaging in a comprehensive planning process that includes strategic planning, firm performance, and ratio analysis appears to be associated with higher levels of firm performance (Williams et al., 2018). However, other researchers have indicated that a formal business plan may be an unnecessary step (Lange et al., 2007). In the context of public assistance programs to promote growth of small businesses in Israel, providing strategic planning assistance, a component of developing a business plan, was not significant related to performance outcomes (Schayek & Dvir, 2011).

But research is unclear as to what happens when levels of business planning interact with levels of opportunity confidence. The entrepreneur may feel as if they have the skills to succeed in the venture, but what happens if they believe that the outcomes of the venture are unfavorable? Or vice versa?

A study with undergraduate students utilizing a scenario-based research design, found evidence suggesting that a low level of uncertainty (such as might be experienced when business planning is occurring) combined with a high level of positive anticipatory emotions would result in an increased tendency to invest more time in the venture (Harvey & Victoravich, 2009). In the context of entrepreneurship, entrepreneurs who regularly engage in business planning would likely reduce their feelings of uncertainty. In addition, they might associate their belief in the long-term viability of their venture with positive anticipatory emotions. Therefore, it might suggest that these reduced feelings of uncertainty (resulting from using a business plan) and increased positive anticipatory emotions (i.e. venture confidence) would increase the tendency of an entrepreneur to escalate commitment (Rita et al., 2018). That said, it seems plausible to argue that use of a business plan might play even a more critical role in the event of low venture confidence. Entrepreneurs who have little belief in their venture survival might be in a more dire need of a business plan to reduce their levels of uncertainty and increase their decision-making confidence. Developing a business plan is associated with higher levels of self-efficacy (Newman et al., 2019). Entrepreneurs with lower levels of venture confidence can doubly benefit from a business plan as an objective tool that gives structure to the business and reduces the uncertainty surrounding the venture survival and as a subjective tool that boosts entrepreneurs’ perceived control over business operations. Therefore, the interaction between business planning and venture confidence more strongly impacts time investment in a venture at lower levels of venture confidence.

Hypothesis 3: Use of a business plan increases the impact venture confidence has on future time invested by the founder, and the increase is higher when venture confidence is low rather than high.

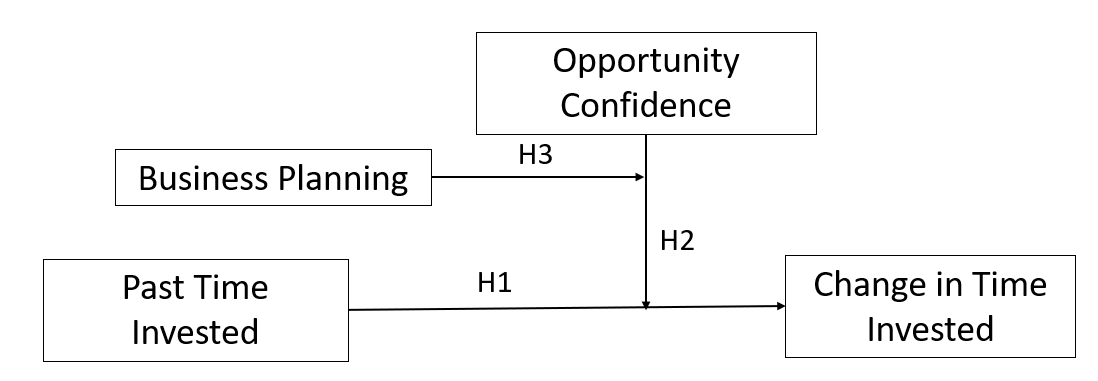

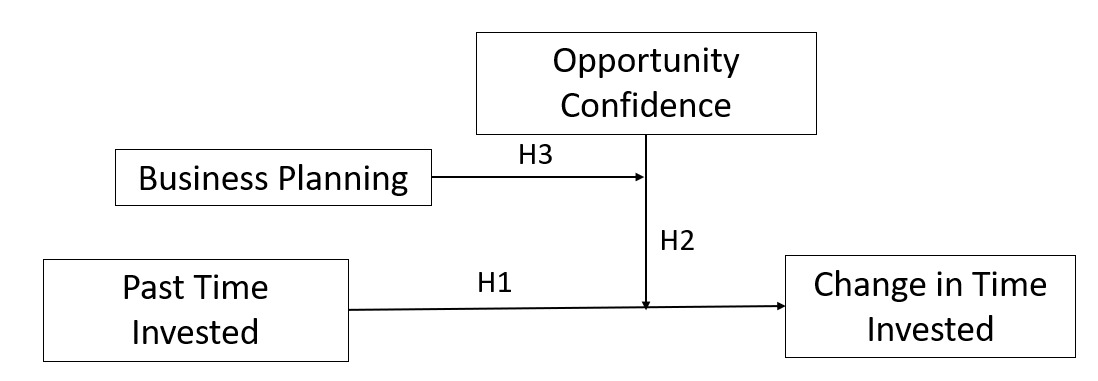

Theoretical Model

The model depicted in Figure 1 shows the relationships set forward in this study.

METHODS

Sample and Data Collection

Data for this project came from the Comprehensive Australian Study of Entrepreneurial Emergence (CAUSEE) longitudinal study. This panel study identified 625 nascent firms and 559 young firms through 30,430 screening interviews. The researchers then collected the data over a five-year effort with waves of data collection occurring each year. This paper only used data from Wave 1 through Wave 4, as Wave 5 did not include data regarding time invested in the venture. After removing organizations where full data was not available, 731 firms remained in the sample. Of these, 351 were solo entrepreneurs, 245 indicated that they had a founding partner, and 226 were part of a founding team. Table 1 includes a full list of the variables from the research effort that are included in this study.

Measures

Time invested. Time invested (ADJtime) was measured by the number of hours spent per week for all active owners divided by the number of active owners. In cases where the data were obviously erroneous, the data point was set to missing (Aguinis et al., 2013). For instance, one company with 5 owners indicated that owners spent a total of 2400 hours per week on the business.

The number of active owners (OWNERS) was missing for 551 out of the 731 nascent ventures. A field indicating total owners limited the survey options to 1, 2, 3, 4, or 5 or more owners. Therefore, we used the total number of active team members where the data was available and the total number of owners where it wasn’t available. Companies that indicated 5+ members were adjusted to 5 owners. For three ventures, ownership variables were not collected until Wave 2. In these cases, we used the Wave 2 data to populate Wave 1. The final three ventures had no ownership information available, so ownership information was left as missing. This procedure was repeated for data from Waves 2 through 4.

Change in time invested. Change in time invested (TCHANGE) was computed by subtracting the amount invested in the prior period versus the amount invested in the current period.

Opportunity Confidence. Opportunity confidence (CONF) is operationalized by the entrepreneur’s perception of the likelihood of the business still operating in five years.

Use of a business plan. Business plan usage (PLAN) is based on a question asking founders whether they referenced a business plan as a means of thinking things through in order to seize opportunities or avoid mistakes.

Control Variables. Due to a relatively small sample size and a model with a moderator and interaction term, only four controls variables were included to maintain an appropriate level of power. These included sales and venture growth (as they would likely impact motivation, and therefore also time investment), as well as the number of active owners, and industry. Sales were measured with a binary variable indicating whether sales were receiving in six of the last twelve months. Venture growth was measured using the entrepreneur’s response to the question related to growth of the company’s value as compared to twelve months previously. In addition, the number of active owners was included to control for effects of having multiple people involved in the venture (Aldrich & Kim, 2007; Howell et al., 2022). Finally, where possible, industry was added to control for industry-related effects, such as certain industries have differing norms related to business plans and financing (Brinckmann et al., 2010). We created dummy variables for each of the 10 industries represented in the data (agriculture, business consulting, communications, construction, consulting services, health and social services, manufacturing, other, retail, and unknown). The following industries had six or fewer companies in the category and were included with the other category: transportation, hospitals, and finance companies. To prevent collinearity, we dropped ‘other’ from the analysis.

RESULTS

Descriptive Statistics. Table 3 includes the means, standard deviations, and correlations for all variables and controls included in the analysis. All variables appeared to have correlations within a reasonable range. Time invested in the venture (time per active owner) ranged from 0 hours to 120 hours per week. Expectations regarding the future of the venture were relatively high with a mean of 83.46% of entrepreneurs reporting they were confident the venture would survive five years.

Hypothesis testing. Hypothesis 1 suggests that past time invested in a venture will lead to an increase in future time invested. To make full use of the available panel data to test Hypothesis 1, we opted to use panel data analysis with Stata 16.1. As time invested in the venture cannot serve as both a dependent variable and predictor variable for panel data analysis, we computed a new variable (ADJtime) to indicate the change in time invested from one period to the next for use as the dependent variable. Based on a statistically significant Hausman test (χ=157.86, ρ<.001), we tested hypothesis 1 using a fixed effects estimator. Table 4 provides the results of the panel data analysis using Stata v 16.1 and indicates that the change in time invested in a nascent venture does appear to be related to past time invested, while controlling for sales, venture growth, and the number of owners) explaining 19.0% of the overall variability in the outcomes (ρ<.001). Within individuals, 53.0% of the variability is explained. Industry was omitted from the calculation due to multicollinearity.

Since measurement of escalation of commitment considers the probability of success, as a robustness check, we ran a linear regression including opportunity confidence as an additional control variable. This model was also significant, with an overall 46.7% of the variance explained (ρ<.001). These results provide support for Hypothesis 1, suggesting that past investments of time in a venture are positively related to future investments in a venture.

Hypothesis 2 suggests that the level of opportunity confidence affects the relationship between past time invested in a venture and the change in time invested. The predictor variable was time invested in the prior period, and the moderator was opportunity confidence (included using an interaction variable computed as confidence times prior time invested). Controls included sales, venture growth, number of active owners, and industry. We calculated power (.99) based on 26 predictors (the IV, moderator, three controls, and 10 industry dummy variables) and a sample size of 650. As shown in Table 4, there was no support for Hypothesis 2.

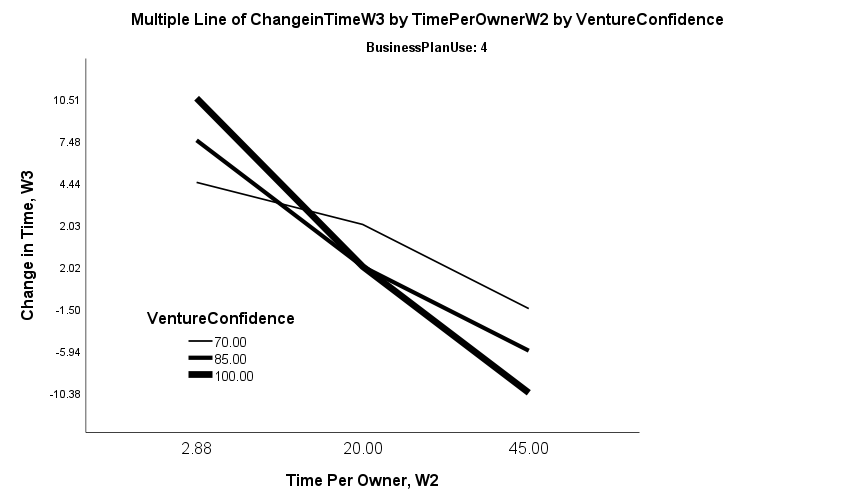

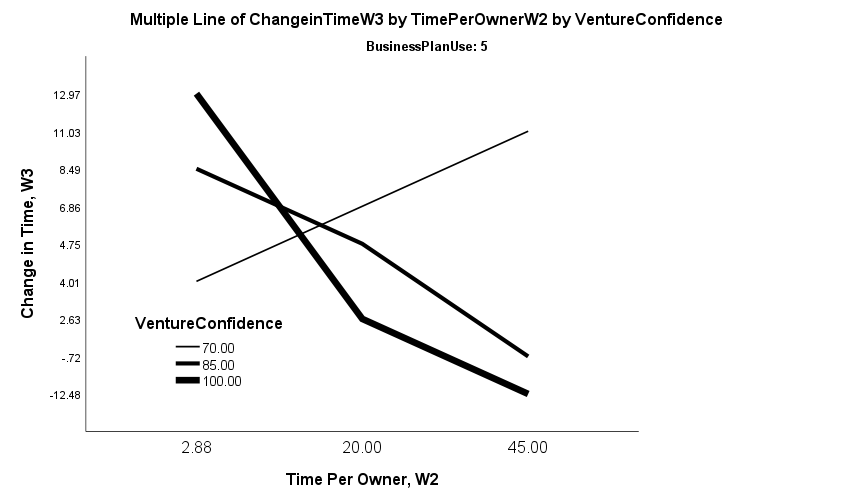

In Hypothesis 3, we sought to determine whether the use of a business plan might change the effect of opportunity confidence on the difference in time invested between one wave of data collection and the next. One of the controls (GROW) was not available during the first wave of data collection, meaning that the change in time between Wave 1 and Wave 2 could not be included. Additionally, including two observations from a single venture would violate the assumption of independence (Osborne & Waters, 2019). Combined with the loss in observations between Wave 2 and Wave 4, we opted to proceed with testing data from Waves 2 and 3, predicting the change in time invested for Wave 3. As the research question suggested moderated moderation, we used Process for SPSS to test Hypothesis 3.

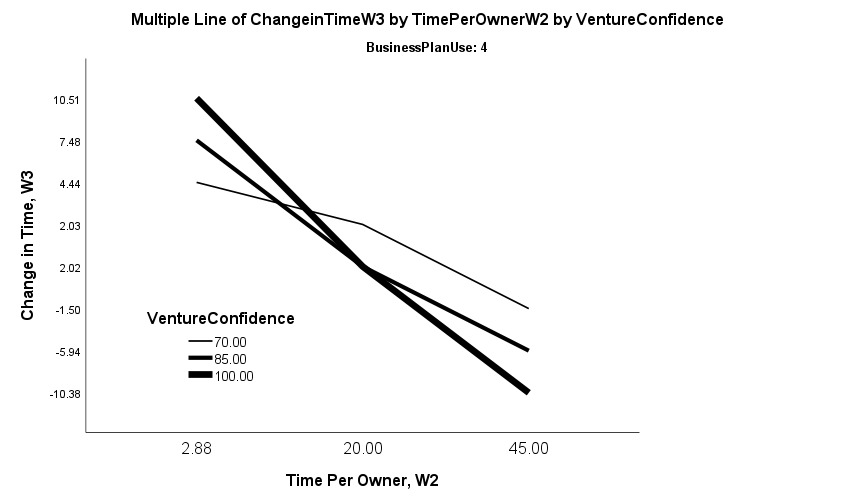

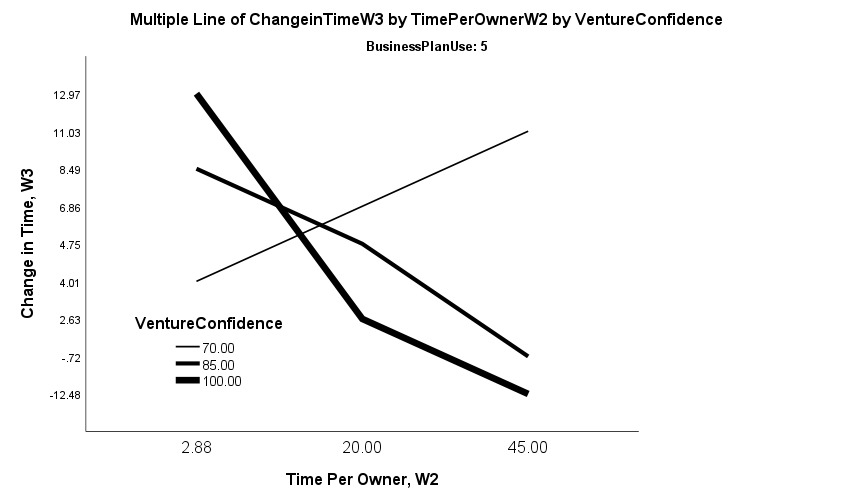

There were 153 cases where time data had been collected in two subsequent time periods. The data did not meet the assumption of homoscedasticity, as the scatterplot of the residuals indicates a distinct pattern. Therefore, moderation analysis using Process was conducted using heteroscedasticity-consistent covariance matrix estimators, following recommendations from Hayes (2018) and Hayes & Cai (2007). Using Process Model 3 in SPSS (results shown in Table 5), this model appeared to account for a significant proportion of the variance in time invested in Wave 3 (R2 = 0.578, p < .001), suggesting that using a business plan affects the moderating effect of opportunity confidence on the relationship between time invested in Wave 2 versus Wave 3 while controlling for sales, venture growth, the number of active owners, and industry. The overall interaction effect was also significant (b=-0.014, p <.001), indicating the data provided support for Hypothesis 3. Examination of the interaction plots in Figures 2 and 3 suggest that the impact of using a business plan on the interaction of opportunity confidence and time invested (weekly) in Wave 2 appears to be greatest when the use of the business plan is high in that those with lower levels of confidence and higher use of a business plan tend to increase their hours invested. This is in contrast to those with higher levels of confidence, who decrease their hours invested regardless of their use of a business plan.

DISCUSSION

Continued time investment in a new venture is a necessary condition for survival and growth of that venture. This is because entrepreneurship is a process that requires consistency and tending (Davidsson & Gruenhagen, 2022; Mcmullen & Dimov, 2013). Moreover, the more time an entrepreneur invests in a venture, the better he/she can develop strategies to deal with the uncertainties surrounding the business. Also, entrepreneurs’ commitment toward their venture (including the time invested in a venture) greatly helps with building credibility in the eyes of stakeholders and securing external financing, when needed (Busenitz et al., 2005). But how might we predict the amount of time an entrepreneur might invest in their venture? This paper suggests that prior time invested, when considered in the context of opportunity confidence and business plan usage provides part of the answer. Specifically, entrepreneurs who use a business plan to make decisions and have lower levels of opportunity confidence are more likely to increase the time invested in the nascent venture at a higher rate.

First, this paper finds a direct positive relationship between the time invested in a venture in the past and the time invested in the future. This finding lends support for escalation of commitment in the context of nascent ventures. Prior research shows that entrepreneurs are prone to this escalation behavior (Kier et al., 2014; McCarthy et al., 1993) which manifests in investing more time and effort in a venture in proportion to the time and effort initially invested, regardless of the anticipated outcome. For purposes of this study, the relationship between past time and future time investments was intended to serve as a baseline and, as such, provides an adequate foundation for the remainder of the paper.

Second, although we did not find support for the relationship between venture confidence and future time investment, our results indicated that there may be conditions which increase or decrease the impact of venture confidence. Indeed, adding the context of actively using a business plan did change the effect of expectations regarding venture success on effort expended on the nascent venture. The most statistically significant model for this impact indicated that those with higher business plan usage tended to increase the rate of hours worked to a less extent when opportunity confidence was high and vice versa. This suggests that business plan use, when combined with high levels of opportunity confidence, may provide a comfort level to the nascent entrepreneur that they do not need to work as many hours. This is as opposed to entrepreneurs with lower levels of confidence in the venture who might believe that they should work harder to increase the probability of their success.

Contributions and Implications. One of the theoretical contributions of this study is shedding light on the controversial relationship between past time and future time invested in a venture. Whereas prior findings have been somewhat inconsistent, this study provides another evidence for the significance of this relationship. Moreover, this study uncovers and delineates conditions under which such relationship might become pronounced or weakened. As was discussed earlier, venture confidence (an individual-level factor) and business plan use (a firm-level factor) can interact and impact how entrepreneurs decide to invest time in their ventures. One can always think of other factors such as entrepreneurs’ motivation levels, past failures, relevant industry experience, and resource endowments as potential moderators of the relationship between past commitment and future time investments. A broader theoretical implication of this study revolves around the notion of entrepreneurship being a temporal journey toward a set goal (Davidsson & Gruenhagen, 2022). The findings of our study provide further evidence for this process view toward entrepreneurship through delineating how successful new venture creation attempts follow a temporal process wherein time invested in one stage contributes to future time investments and progress in a later stage.

This study also has practical implications regarding the differing impact of using a business plan on those entrepreneurs with low venture confidence versus high venture confidence. Entrepreneurship is unpredictable and requires continued time commitment to be successful. An entrepreneur with high venture confidence might benefit from a reminder of the importance of not cutting back on time, even when the venture team is making use of their business plan and the venture is expected to succeed. On the other hand, an entrepreneur with low venture confidence might be overly reliant on a belief in their business plan to overcome the obstacles that they see. In this case, the entrepreneur might benefit from being deliberate with the way they develop their business plan. These entrepreneurs need to first identify in what areas they deem the business to be struggling and then tailor a plan that most effectively addresses those specific areas (be it the core value proposition, target market selection, long-term viability/profitability, etc.).

Limitations. Panel data, while ideal for determining causality, also causes potential issues related to selection and survival bias. Selection bias in that people must first opt into the study and then continue through additional waves of data collection. Survival bias in that some nascent ventures do not continue, and therefore do not participate in additional waves of data collection. It is possible that this may have impacted the results of this study.

An alternate explanation for these results might center around self-control, which is quite similar to perceived behavioral control. When an entrepreneur is being disciplined and using a business plan to drive their work, it may begin to deplete their reserve of self-control. An experiment with undergraduate students (DeBono & Muraven, 2013) found that those students who completed an exercise requiring self-control were able to make better predictions regarding the success of a venture. Therefore, it is possible that entrepreneurs with depleted self-control, through the disciplined use of a business plan, may lead to more accurate predictions regarding the likelihood of their venture surviving. This change in belief will likely also impact the amount of time an entrepreneur continues to invest in their venture. Due to limitations in data availability, there was no way to test this alternate hypothesis.

Future Research. Based on these findings, there are several opportunities for future research. First, there might be cognitive or sociological factors that lead to using a business plan that also affects decisions related to time investment. For instance, entrepreneurs with higher levels of self-efficacy are more likely to engage in planning activites (Brinckmann & Kim, 2015). Future research might seek to determine whether self-efficacy also leads to higher levels of time investment. Second, researchers could explore whether similar results might be obtained using planning mechanisms other than a formal business plan. For instance, the Lean Startup methodology suggests that formal business plans do not allow the flexibility required by new ventures, and therefore proposes a one page business model canvas instead (Bortolini et al., 2021). As the business model canvas is much more fluid, the effect on venture confidence and time investment may be different than that of a traditional business plan that is typically more static. A third potential avenue to pursue could be to clarify how the use of a business plan, combined with the additional (or lower) time investment, might impact the eventual outcome of the venture. Research to-date on the direct effect has been inconclusive (Müller et al., 2023), so further clarification is needed. Finally, future research can seek to identify the mechanism through which the decision to invest more (or less) time in the venture is made. The prior may, in part, be driven by the desire of an entrepreneur to retain their identity as entrepreneur, as the entrepreneur might fear that failure may lead to the abandonment of who they see themselves to be. Shepherd and Haynie (2009) suggest that entrepreneurs face a strong desire to meet needs of distinctiveness and, at the same time, feelings of belonging. It could be that, to maintain their distinct identity as an entrepreneur, the founder could do so in contradiction of evidence that the venture is unlikely to succeed. Grimes (2018) also finds that an aversion to loss of their identity as an entrepreneur might cause the entrepreneur to make decisions that appear contrary to predictions of the level of success of the venture.